You have 0 items in your cart

Why Every Adult Needs to Understand the General Durable Power of Attorney

A general durable power of attorney is a legal document that gives someone you trust broad authority to manage your finances and property, even if you become mentally incapacitated. Unlike a regular power of attorney that ends when you lose mental capacity, the “durable” feature means it continues working when you need it most.

Quick Overview of General Durable Power of Attorney:

- What it is: Legal document granting broad financial powers to a trusted agent

- Key feature: Remains valid even if you become incapacitated

- Powers granted: Banking, real estate, investments, tax matters, and more

- When it ends: Upon your death, revocation, or agent resignation

- Requirements: Must be signed while mentally competent, typically notarized

- Agent duties: Must act in your best interest and keep detailed records

Without this document, your family faces costly court proceedings called guardianship just to pay your bills or manage your assets. A general durable power of attorney prevents this nightmare scenario while giving you complete control over who makes these critical decisions.

The stakes are high. Whether you’re a business owner protecting your company’s future or a parent ensuring your family’s financial security, understanding this document could save you thousands in legal fees and months of court delays.

I’m Michael Hurckes, Managing Partner at Ironclad Law, where I’ve helped countless clients steer complex estate planning and general durable power of attorney issues throughout my career in litigation and financial services law.

Quick general durable power of attorney definitions:

- living will and durable power of attorney

- simple will and power of attorney

- power of attorney revocable trust

What Is a General Durable Power of Attorney?

A general durable power of attorney (GDPOA) is a legal document that lets you hand over broad financial and property management powers to someone you trust—known as your agent or attorney-in-fact. The “general” part means these powers cover just about everything: from paying your bills and selling your house to handling your taxes or managing investments. The “durable” part is what gives this document its muscle: it stays effective even if you become mentally incapacitated.

The principal is you—the person granting authority. The agent (attorney-in-fact) is the individual you name to act for you. The durability clause ensures your power of attorney remains valid if you lose mental capacity. Without that language, the document would simply shut off when you need it most.

Without a general durable power of attorney, your family could be locked out of your accounts, unable to pay your bills, or forced to go to court for permission—an expensive and stressful ordeal.

How a General Durable Power of Attorney Differs from a General Power of Attorney

A basic general power of attorney lets your agent help you only while you have mental capacity. The moment you become incapacitated, it ends. A general durable power of attorney keeps working through incapacity. The key difference is the durability language, which must be spelled out in the document.

Think of it this way: a GPOA is great for short-term needs (like when you’re traveling), but the GDPOA is your safety net for long-term planning. Both end if you pass away.

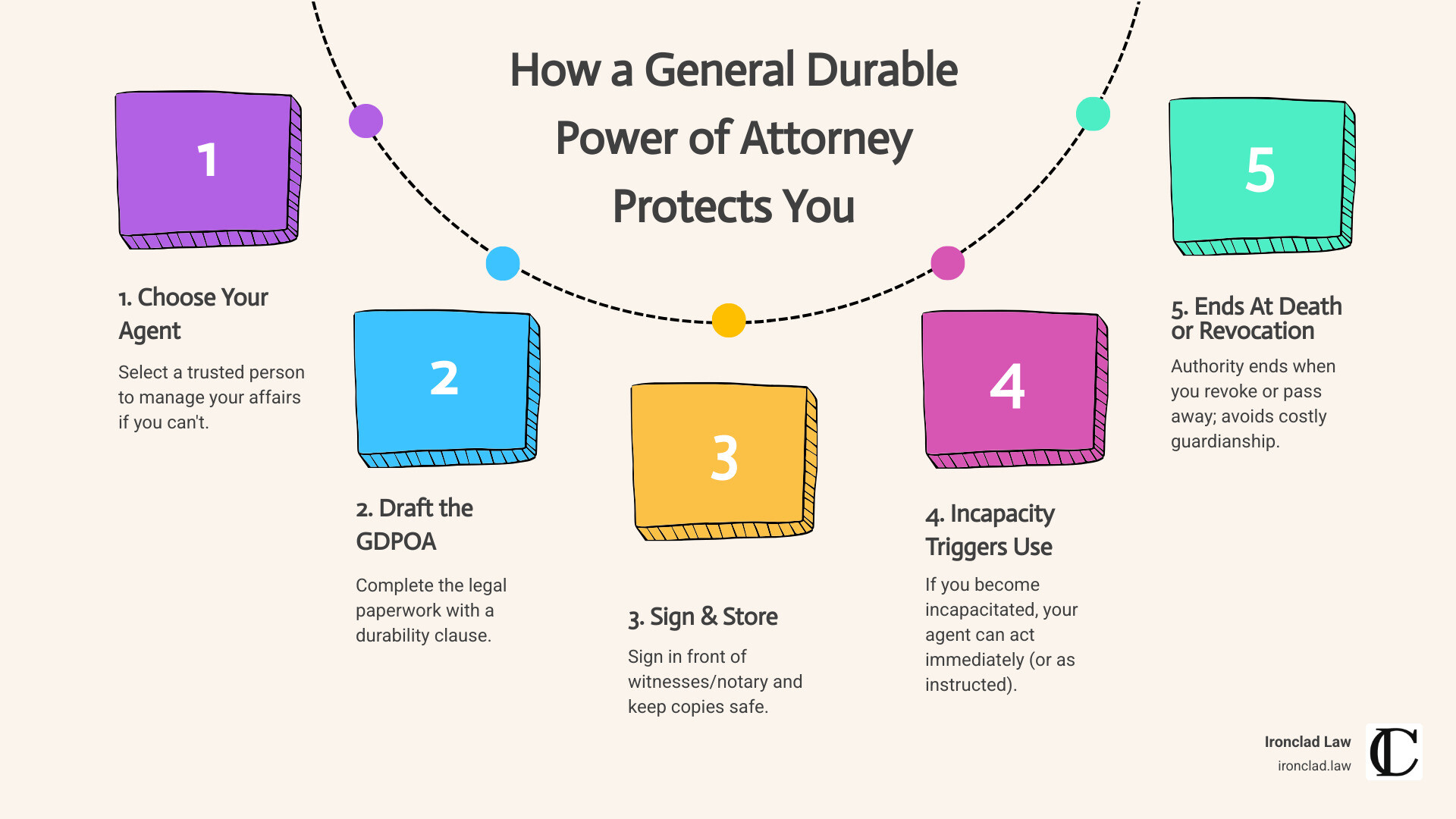

When Does a General Durable Power of Attorney Take Effect and End?

A general durable power of attorney can take effect in two main ways:

- Immediate: Powers start as soon as you sign. Your agent can help right away.

- Springing: The document only “springs” into action if a specific event happens—usually, if a doctor certifies that you’ve become incapacitated.

It ends at your death, if you revoke it while you have capacity, if your agent resigns and you don’t name an alternate, if you’re bankrupt (in some states), or if a court declares it invalid.

For more details about how this document fits into your overall estate plan, check out our living will and durable power of attorney resource.

Powers and Responsibilities of Your Agent

When you sign a general durable power of attorney, you’re handing over the keys to your financial kingdom. Your agent can step into your shoes and handle almost any money matter you could handle yourself—unless you specifically say otherwise.

Your agent can manage your bank accounts and pay your bills, buy, sell, or refinance real estate, handle investments and retirement accounts, file your taxes and deal with the IRS, collect government benefits like Social Security, and manage all your personal finances.

Legal Duties Under a General Durable Power of Attorney

Your agent has serious legal duties that come with serious consequences if they mess up.

The best-interest standard is the golden rule. Your agent must always act in your best interests, not their own. This is called fiduciary duty.

Separate accounts are non-negotiable. Your agent cannot mix your money with their money. This rule exists because mixing money is often the first step toward “borrowing” money that never gets paid back.

Accurate recordkeeping is crucial. Your agent needs to keep receipts, bank statements, and detailed records of every transaction.

Gift limits are another important boundary. Most states don’t allow agents to give away your money—even to family members—unless you specifically authorize it in your general durable power of attorney.

For more detailed information about these responsibilities, check out Power of Attorney responsibilities.

Monitoring & Holding an Agent Accountable

Third-party oversight is one of the smartest safeguards you can build into your plan. You might name a trusted family member or friend to review your agent’s decisions periodically.

Co-agents can provide another layer of protection. You can require two people to agree on major decisions, like selling real estate or making large withdrawals.

Periodic reporting requirements can keep your agent honest. You might require them to provide quarterly financial statements to your family or attorney.

Court intervention is the nuclear option. If family members suspect abuse, they can ask a court to review the agent’s actions. Courts can remove bad agents, require them to pay back stolen money, or even pursue criminal charges.

Elder financial abuse costs Americans billions of dollars every year. You can learn more about this issue from scientific research on elder financial abuse.

Creating and Customizing Your General Durable Power of Attorney

State Forms, Witnessing, and Notarization

Setting up a general durable power of attorney isn’t as simple as filling out a one-size-fits-all form—every state has its own rules. You’ll need to sign your GDPOA while you’re still mentally sharp. Most states require at least one or two adult witnesses, and it’s almost always best to have the document notarized—especially if your agent might handle real estate. Some states offer official forms, while others give you more freedom to customize. Be sure your power of attorney includes the right statutory “durability” language so it keeps working if you lose capacity.

Step-by-Step Drafting Guide

Start by choosing someone you trust—pick an agent who’s reliable and good with details and money. Next, decide exactly what powers you want your agent to have. You can give them broad authority, or keep it limited to specific tasks.

Include a clear durability clause, such as “This power of attorney shall not be affected by my subsequent incapacity.” This keeps your document valid when you need it most.

Decide when your agent’s powers start. Should the authority be effective immediately, or only if a doctor says you’ve lost capacity (springing)?

Name one or more alternate agents—your first choice might be unavailable someday. After finalizing your choices, follow your state’s requirements for signing, witnessing, and notarization. Store the original in a safe place and give copies to your agent, alternates, and anyone else who needs to know.

For a deeper dive, our Estate and Trust Planning guide walks you through more details.

Limiting or Expanding Authority

You can limit authority—maybe your agent can act only on real estate, or you want to block large gifts without your written permission. You can also carve out health decisions (using a separate healthcare power of attorney), or require that your GDPOA only “springs” into action if you become incapacitated.

You might want to expand powers to include business interests, or set other special instructions that reflect your wishes. Don’t be afraid to customize—your life and assets are unique. For more about how these documents work together, check out our Living Will and Durable Power of Attorney resource.

Safeguards, Revocation, and Updates

Life changes, and so should your general durable power of attorney. You maintain complete control over this document as long as you have mental capacity. Whether you’re moving to a new state, going through a divorce, or simply want to change agents, you have options.

Written revocation is your best protection. Never rely on verbal instructions. Banks and investment firms need clear, documented proof that you’ve revoked an old power of attorney. A simple letter stating “I hereby revoke all previous powers of attorney” can prevent serious problems.

Don’t forget to destroy the old copies and notify everyone who matters. Your bank, financial advisor, insurance company, and anyone else who has a copy needs to know it’s no longer valid.

Regular reviews keep you protected. I recommend reviewing your general durable power of attorney every three to five years, or whenever major life events occur.

Divorce can automatically affect your GDPOA. In many states, naming your spouse as agent becomes invalid upon divorce. Check your state’s laws and update your documents accordingly.

Revoking or Amending a General Durable Power of Attorney

Timing is everything when revoking a GDPOA. You must have mental capacity to make the revocation legally effective. Plan ahead while you’re still sharp and capable.

The safest approach is creating a new document. When you draft a new general durable power of attorney, include clear language stating that it revokes all previous powers of attorney.

Written notice protects everyone involved. Send formal written notice to your old agent, any backup agents, and all financial institutions. Keep copies of these notices for your records.

Consider filing with your county clerk to create a public record, especially important for real estate transactions or if you’re concerned about potential disputes.

Get professional help for complex situations. If you’re revoking a GDPOA because of suspected abuse or family conflicts, don’t go it alone.

Learn more about coordinating your power of attorney with other estate planning tools at Power of Attorney Revocable Trust.

State-to-State & International Considerations

State laws vary significantly when it comes to power of attorney requirements. What works in Florida might not be sufficient in New York, and vice versa.

Florida takes a strict approach. Under Florida Statute 709.08, you need proper witnessing and notarization for your GDPOA to be valid.

New York prefers its short-form power of attorney. New York has specific statutory language and formatting requirements.

Moving between states requires careful planning. A properly executed GDPOA from one state is generally valid in another state, but some institutions may be hesitant to accept out-of-state documents.

International use gets complicated quickly. If you own property abroad, you may need additional documentation. A Hague Apostille certificate can authenticate your document for use in countries that participate in the Hague Convention.

Don’t assume your document will work everywhere. Some foreign banks may require their own forms or additional certifications.

For professional notarization services, especially for international use, consider Power of Attorney Notary Services.

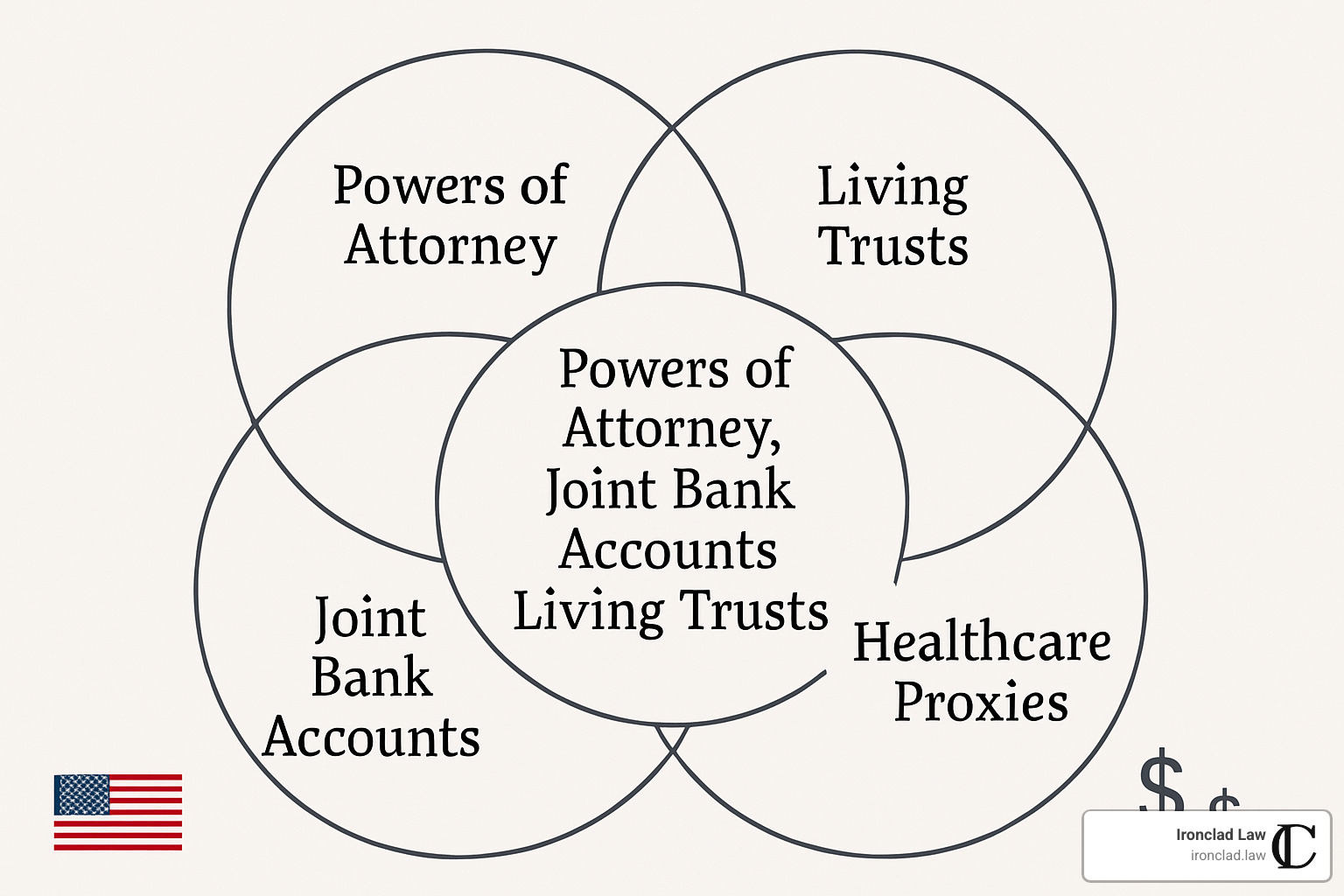

General Durable Power of Attorney vs. Other Planning Tools

When it comes to safeguarding your finances in case of incapacity, a general durable power of attorney (GDPOA) is just one part of the estate planning puzzle. Let’s see how it measures up against other common tools.

Some people think adding a family member to a joint bank account solves everything. It gives instant access to pay bills, but joint accounts mean each owner can take out money at any time, and when you pass, that money may go directly to the surviving owner, leaving your intended heirs out. If you want accountability, a GDPOA is almost always the wiser choice.

A living trust is another option for managing assets if you’re incapacitated. While a trust can seamlessly handle property, it’s more complex and costly to set up than a GDPOA. Trusts are great for avoiding probate and handling larger estates, but they don’t cover everything day-to-day.

A healthcare proxy lets someone make medical choices for you, but it stops at finances. For true protection, you need both types of documents working together.

If you don’t have any of these documents and become incapacitated, your loved ones may face a court-imposed guardianship. That process is slow, expensive, and takes decisions out of your family’s hands.

Beneficiary designations only take effect when you die. They don’t help at all during your lifetime if you’re unable to manage your affairs.

Want to dive deeper? Here’s more on the Power of a lawyer – general power of attorney.

When a Joint Account Makes Sense—and When It Doesn’t

Pros include instant access to pay bills and no court process if one owner dies. But the cons are serious: either party can empty the account at will, accountability is tricky, and you could create tax or inheritance issues for your heirs.

The bottom line? A general durable power of attorney gives you control and oversight—something a joint account simply doesn’t offer.

Complementary Documents for Complete Protection

While a GDPOA is essential, it works best alongside other documents. For full peace of mind, consider adding a living will for your end-of-life wishes, a HIPAA release so your agents can access medical records, a healthcare proxy for medical choices, and a revocable living trust if your estate is more complex. Don’t forget payable-on-death (POD) titles for certain accounts.

You can read more about combining these tools at Simple Will and Power of Attorney.

Frequently Asked Questions about the General Durable Power of Attorney

You probably have questions about how a general durable power of attorney works in real life. Here are the most common concerns I hear from clients, along with straightforward answers that can help you make informed decisions.

Can my agent change my will or beneficiaries?

No, your agent cannot change your will. That’s a hard line in the law—wills can only be changed by you, while you have mental capacity.

But here’s where it gets a bit more complicated: some general durable power of attorney documents do allow agents to change beneficiary designations on things like life insurance policies, retirement accounts, or bank accounts. However, this power must be specifically written into your document. It’s not automatic.

Even if you give your agent this authority, they’re still bound by strict fiduciary duties. They must act in your best interests, not their own. If they change beneficiaries to benefit themselves or act against your known wishes, they can face serious legal consequences.

My advice? Be very careful about granting this power. If you do include it, make sure your document includes clear guidelines about when and how it can be used.

What happens if I don’t have a GDPOA and become incapacitated?

This is where things get expensive and complicated fast. Without a general durable power of attorney, your family will likely need to go to court to get permission to manage your affairs through a process called guardianship or conservatorship.

Here’s what that looks like: Your spouse or adult children have to hire a lawyer, file court papers, and prove to a judge that you’re incapacitated and need help. The court may require medical evaluations, background checks, and ongoing supervision. The whole process becomes public record.

The real kicker? The court might not appoint the person you would have chosen. They could pick a family member you don’t trust, or even a professional guardian who doesn’t know you at all.

This process typically costs thousands of dollars and can take months to complete. Meanwhile, your bills aren’t getting paid, and your family can’t access your accounts to handle basic needs.

Is a GDPOA valid in another state or country?

Most states will honor a properly executed general durable power of attorney from another state, but banks and other institutions sometimes get nervous about out-of-state documents. They may ask for additional documentation or refuse to accept it altogether.

When you’re moving to a new state or buying property elsewhere, it’s smart to update your documents to meet local requirements. Each state has slightly different rules about witnessing, notarization, and specific powers that can be granted.

For international use, things get more complex. Many countries require additional legal certification, like a Hague Apostille, to recognize foreign legal documents. Some countries don’t recognize U.S. powers of attorney at all and require their own equivalent documents.

If you have property or business interests abroad, or if you’re planning to retire internationally, talk to a lawyer who understands both U.S. and foreign requirements. The last thing you want is to find your carefully planned documents are worthless when you need them most.

Conclusion & Next Steps

A general durable power of attorney is more than paperwork—it’s genuine peace of mind for whatever life brings. By putting these safeguards in place now, you decide who will have the authority to step in and manage your finances if you ever can’t. As we’ve discussed, this single document can save your loved ones from court delays, high legal costs, and a whole lot of stress.

At Ironclad Law, we understand that these choices aren’t just legal—they’re personal. We help clients across Florida, New York, and beyond create, review, and enforce strong, reliable powers of attorney every day. Whether you’re planning ahead for your family, running a business, or facing a tough situation, our assertive approach means your interests are always protected.

If you want to future-proof your finances and protect the people you care about, now is the best time to act. Take a close look at your current power of attorney and estate planning documents. If you haven’t reviewed them in a while—or if you’ve never put a plan in place—consider scheduling a consultation with an experienced estate planning attorney. Life changes fast, and your legal documents should keep up.

For more information about your next steps, visit our Estate Planning Needs page. You can also reach out to us directly to get started. Your decisions today shape your tomorrow—and with the right legal tools, you stay in control no matter what comes your way.

This article is for informational purposes and is not legal advice. Every situation is unique—please consult a qualified estate planning attorney for guidance custom to your needs.