You have 0 items in your cart

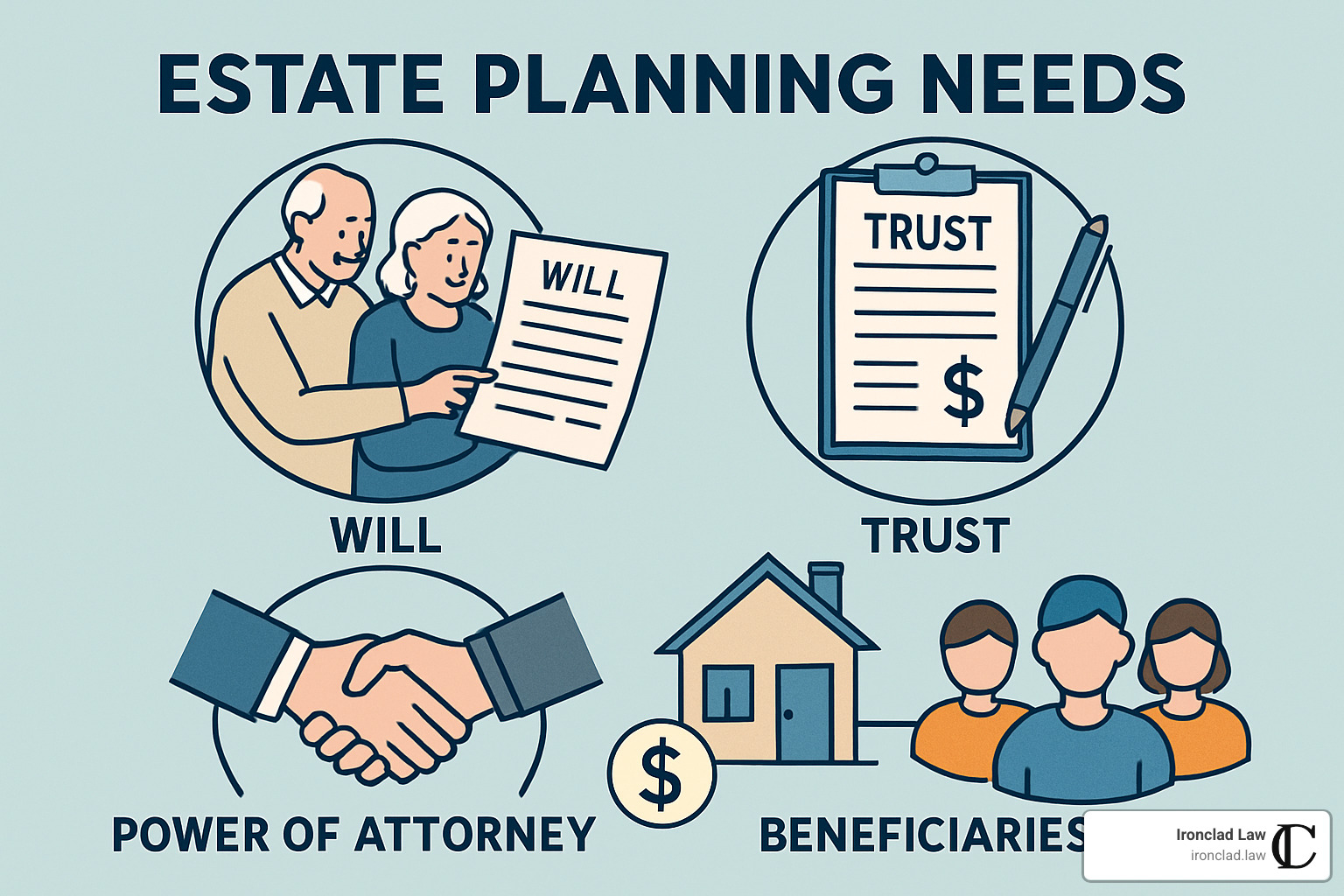

Understanding Your Essential Estate Planning Needs

Estate planning needs include creating a will, establishing trusts, designating powers of attorney, naming beneficiaries, preparing healthcare directives, appointing guardians for minors, managing digital assets, minimizing taxes, and planning for business succession. Here’s what most people need:

- Will or Trust: Legal document directing asset distribution

- Durable Power of Attorney: Someone to manage finances if you’re incapacitated

- Healthcare Directives: Instructions for medical decisions

- Beneficiary Designations: For retirement accounts, insurance policies

- Guardian Nominations: For minor children

- Asset Inventory: Comprehensive list of what you own

Estate planning isn’t just for the wealthy or elderly. Roughly half of Americans don’t have even a basic will, leaving their assets and loved ones vulnerable to court decisions they might not have wanted. Creating a comprehensive estate plan gives you control over what happens to everything you’ve worked for and ensures your family is protected.

Without proper planning, your assets could be tied up in probate for over a year, with fees potentially consuming up to 5% of your estate’s value. More importantly, without documenting your wishes, you lose control over healthcare decisions if incapacitated and how your assets are distributed after death.

I’m Michael Hurckes, Managing Partner at Ironclad Law with extensive experience helping clients address their estate planning needs through personalized strategies that protect assets and provide peace of mind. My background in financial services regulation and family law provides a unique perspective on how to create comprehensive estate plans that truly protect what matters most.

Estate planning needs basics:

– medicaid estate planning

– power of attorney revocable trust

– special needs estate planning attorney

Top 12 Estate Planning Needs You Can’t Ignore

Many folks think a simple will covers all their estate planning needs, but there’s so much more to protecting your legacy. I’ve seen too many families find critical gaps in their plans during the worst possible moments. A truly comprehensive approach addresses not just what happens after you’re gone, but also protects you and your loved ones during your lifetime.

Here’s what you absolutely can’t afford to overlook, whether you’re just starting out or already have substantial assets:

Your estate planning needs checklist should include wills that direct asset distribution and guardian nominations, and trusts that can provide privacy and avoid probate. Don’t forget powers of attorney for financial matters if you become incapacitated, and properly updating beneficiary designations on accounts that pass outside your will.

A complete plan also addresses healthcare with a living will and medical directives, and includes guardianship arrangements for minor children. In our digital age, planning for digital assets like online accounts and cryptocurrencies is essential.

Smart tax planning strategies can preserve more of your wealth for heirs, while probate avoidance techniques save time and money. Business owners need succession planning to ensure their company survives their passing, and many find charitable giving strategies that create lasting legacies while providing tax benefits.

Each of these elements serves a specific purpose in your overall protection strategy. At Ironclad Law, we’ve found that addressing these twelve critical areas creates a fortress around what you’ve built and those you love. In the following sections, we’ll explore each component in detail, starting with something surprisingly basic but often overlooked: knowing what you actually own.

1. Inventory Your Assets

I remember sitting with a client who insisted she “didn’t have much” to her name. By the end of our asset inventory session, she was genuinely surprised at how much she’d accumulated over her lifetime. This happens more often than you might think!

Creating a thorough inventory is the foundation of addressing your estate planning needs. Think of it as taking a complete snapshot of your financial life – without this picture, it’s impossible to create a plan that truly protects everything you’ve worked for.

Your asset inventory should capture three key categories:

Tangible assets are the things you can physically touch – your home, that vintage car in the garage, grandma’s jewelry, artwork hanging on your walls, furniture, and other physical possessions that hold both financial and sentimental value.

Intangible assets might be less visible but often represent significant value – bank accounts, investment portfolios, retirement plans (401(k)s, IRAs), life insurance policies, ownership interests in businesses, intellectual property like patents or copyrights, and increasingly important digital assets like cryptocurrency.

Don’t forget to document your liabilities too – outstanding mortgages, auto loans, credit card balances, and other debts that will need to be addressed when settling your estate.

At Ironclad Law, we’ve developed a simple but comprehensive process to help you track down assets you might have forgotten about. Many clients find accounts or possessions they’d completely overlooked – sometimes with significant value attached. This thorough inventory becomes an invaluable resource for your executor or trustee, giving them a roadmap to locate and manage everything you own when the time comes.

What you don’t inventory, you can’t properly protect in your estate plan. This crucial first step ensures nothing falls through the cracks.

2. Draft a Last Will & Testament

Let’s face it—none of us likes thinking about our own mortality. But creating a will is perhaps the most fundamental step in meeting your estate planning needs. Think of your will as your final voice, ensuring your wishes are heard loud and clear when you’re no longer here to express them yourself.

A will isn’t just about who gets your grandmother’s china or your baseball card collection. It’s a powerful legal document that provides critical instructions about everything you care about.

When I sit down with clients at Ironclad Law, I always emphasize these essential elements of a solid will:

Your will should clearly name the people or organizations who’ll receive your assets—and exactly what they’ll get. It should appoint a trusted executor (with backups) who’ll handle everything from paying final bills to distributing keepsakes. If you have children under 18, your will is where you nominate guardians who’ll raise them according to your values.

Don’t forget those personal items that might not be worth much financially but mean the world emotionally. Many family conflicts arise over sentimental items that weren’t specifically addressed. And for many of us, our pets are family too—your will can include provisions for their care.

Here’s what happens without a will: your state essentially writes one for you through intestacy laws. In New York, for instance, if you have a spouse and children, your spouse gets the first $50,000 plus half of what’s left, with your children splitting the remainder—regardless of your children’s ages or your actual wishes. The court will also appoint someone to serve as your executor and, if necessary, as guardian for your minor children.

Is that really how you want your life’s story to end—with the state making these deeply personal decisions for you?

A properly drafted will ensures your voice is heard, your loved ones are cared for, and your legacy is preserved exactly as you intend. It’s not just a document—it’s your final act of love and responsibility for the people and causes you care about most.

3. Set Up a Revocable Living Trust

“But I already have a will—isn’t that enough?” This is one of the most common questions we hear at Ironclad Law. While a will is certainly essential, a revocable living trust offers powerful advantages that many of our clients find invaluable once they understand them.

Think of a revocable living trust as your will’s more private, efficient cousin. Unlike a will, which becomes public record during probate (meaning anyone can read about who got what), a trust keeps your family’s financial matters confidential. This privacy protection alone is why many of our clients choose to establish one.

But privacy is just the beginning of what makes a trust so valuable. When assets are properly placed in your trust—a process we call “funding”—they can bypass the probate court entirely. This means your loved ones gain access to their inheritance months or even years sooner than they would through probate, and without the associated court costs that can eat away at your estate.

Perhaps most importantly, a revocable living trust shines as an estate planning need when it comes to incapacity planning. If you become unable to manage your affairs due to illness or injury, your designated successor trustee can step in seamlessly to handle your finances—no court intervention required.

The beauty of this trust type is right in the name—”revocable” means you maintain complete control during your lifetime. You can add assets, remove them, change beneficiaries, or even dissolve the trust entirely if your circumstances change.

Your trust works alongside your will rather than replacing it. Your will can direct any forgotten assets into your trust through what we call a “pour-over” provision, creating a safety net for comprehensive coverage.

Want to learn if a revocable living trust makes sense for your situation? We’re happy to walk you through the details and help you decide.

More info about revocable trust services

4. Why Beneficiary Designations Top Your Estate Planning Needs

When clients come to us at Ironclad Law, they’re often surprised to learn that their carefully crafted will might not control where all their assets go. That’s because beneficiary designations actually trump what’s written in your will—making them one of the most critical yet frequently overlooked components of your estate planning needs.

Think of beneficiary designations as direct passes that allow certain assets to bypass probate entirely. These special forms determine exactly who receives your life insurance proceeds, retirement funds, and other specific accounts when you pass away—regardless of what your will says.

Your most important accounts with beneficiary designations include your life insurance policies, which provide immediate financial support to your loved ones, and retirement accounts like 401(k)s, IRAs, and pension plans that you’ve likely spent decades building. Many people don’t realize that payable-on-death (POD) bank accounts and transfer-on-death (TOD) investment accounts also work this way. In some states, you can even create transfer-on-death deeds for real estate, allowing your home to pass directly to heirs without probate.

I’ve seen heartbreaking situations where outdated beneficiary forms sent substantial assets to ex-spouses, completely unintentionally. In other cases, children born after the forms were completed were accidentally excluded from inheriting. One client was devastated to learn her father’s $500,000 life insurance policy went to an aunt he hadn’t spoken to in 20 years—simply because he never updated the form after reconciling with his family.

The solution is simple but requires diligence: review all your beneficiary designations after every major life event—marriages, divorces, births, deaths—and at minimum every five years. Keep copies of the current designations with your estate planning documents, and make sure your loved ones know where to find them.

These designations aren’t just paperwork—they’re powerful tools that ensure your hard-earned assets reach exactly who you intend, exactly when they need them most.

5. Execute a Durable Financial Power of Attorney

Let’s talk about something many people overlook until it’s too late – who will handle your finances if you can’t. A durable financial power of attorney might sound like legal jargon, but it’s actually one of your most important estate planning needs.

Think of it as your financial safety net. Without this crucial document, your loved ones might find themselves in court seeking guardianship – a process that can drain thousands from your savings and take months while bills pile up unpaid.

Your financial power of attorney gives someone you trust (your “agent”) the authority to step into your financial shoes when needed. This person can pay your mortgage, handle your tax returns, manage your investments, and even run your business if necessary. They become your financial voice when you can’t speak for yourself.

At Ironclad Law, we’ve seen how this simple document prevents financial disaster. One client suffered an unexpected stroke at 52, but because she had a proper DPOA in place, her husband could immediately access their accounts to pay medical bills and keep their household running without missing a beat.

We always recommend naming not just a primary agent but at least one backup person too. Life happens – your first choice might be unavailable or unwilling to serve when the time comes. Having alternates ensures you’re covered no matter what.

The beauty of this document is its flexibility. We can customize it to match your comfort level – from limiting authority to specific transactions to granting comprehensive powers. You might want your agent to manage everything except your business, or perhaps you’d prefer they consult with your financial advisor before making investment decisions. Whatever your preference, we can craft language to reflect it.

Without this document, even your spouse may struggle to access accounts in your name alone. Banks and investment companies have strict privacy rules that a power of attorney helps overcome.

While we hope you never need to use this document, having it ready provides invaluable peace of mind. Like insurance, it’s better to have it and not need it than need it and not have it. Your future self – and your family – will thank you for this bit of thoughtful preparation.

6. Create Health Care Directives & Living Will

Let’s talk about something none of us enjoy thinking about, but that brings incredible peace of mind once addressed. Healthcare directives are among the most compassionate estate planning needs you can fulfill—not just for yourself, but for those who love you.

Imagine your family gathered in a hospital waiting room, overwhelmed with emotion and suddenly faced with critical decisions about your care. Without clear instructions, they’re left guessing what you would want while managing their own grief and stress. I’ve seen this scenario play out too many times, and it’s precisely why healthcare directives matter so much.

Your healthcare planning toolkit should include three essential documents:

A healthcare power of attorney (sometimes called a healthcare proxy) names someone you trust to make medical decisions when you can’t speak for yourself. Choose someone who knows your values, can stay calm under pressure, and will advocate for your wishes even when emotions run high.

Your living will (or advance directive) spells out your preferences for life-sustaining treatments. Would you want to be placed on a ventilator? Would you want artificial nutrition if you couldn’t eat? These aren’t easy questions, but answering them now prevents your loved ones from having to guess later.

Don’t forget a HIPAA authorization form, which allows doctors to share your medical information with designated individuals. Without this document, even your spouse might be denied access to crucial information about your condition.

Here’s something many don’t realize: studies consistently show that family members incorrectly predict a patient’s end-of-life care preferences about 30% of the time. That’s why having a heart-to-heart conversation with your healthcare agent is just as important as signing the paperwork. At Ironclad Law, we encourage clients to discuss specific scenarios and values, not just general preferences.

These documents aren’t just for older adults. A 25-year-old in a car accident needs healthcare directives just as much as an 85-year-old with chronic illness. The need for clarity about your medical wishes isn’t age-dependent—it’s human.

7. Name Guardians & Backup Guardians for Minors

If you’re a parent of young children, this might be the most heart-wrenching part of your estate planning needs – but also the most crucial. Without proper guardian designations, a judge who doesn’t know your family will decide who raises your children if both parents pass away. That thought alone keeps many parents up at night.

I’ve seen the relief wash over parents’ faces when we finalize this decision. It’s like setting down a heavy weight they didn’t realize they were carrying. At Ironclad Law, we guide parents through this delicate process with compassion and thoroughness.

When selecting guardians, take time to reflect on who truly aligns with your parenting approach. Consider their values and how they interact with your children today. Do they share your educational priorities, religious views, or discipline style? Someone might be a wonderful aunt or uncle for weekend visits but not equipped for full-time parenting.

Practical considerations matter too. Your sister might be perfect in every way, but if she lives across the country, your children would face the additional trauma of changing schools and leaving friends during an already difficult time. Similarly, your aging parents might have the perfect values but lack the physical energy to raise young children.

Many parents don’t realize they can separate the roles of physical guardian (who raises the children) from financial guardian (who manages their inheritance). This can be ideal when, for instance, your brother is wonderful with your kids but terrible with money.

Perhaps most important is naming backup guardians. Life circumstances change, and your first choice might be unable to serve when needed. We recommend naming at least two alternates to ensure your children never fall into the court system’s default process.

Beyond the legal documents, I always suggest creating a personal letter of intent for your chosen guardians. This isn’t legally binding but provides invaluable guidance about your parenting philosophy, children’s routines, medical needs, and hopes for their future. These personal touches help your guardian make decisions that honor your wishes and provide continuity during a turbulent time for your children.

Court oversight will still be involved to finalize guardianship arrangements, but having your clear intentions documented gives the court strong direction and typically streamlines the process considerably.

8. Fund a Special Needs Trust

When you have a loved one with special needs, their future care becomes one of your most pressing estate planning needs. Many families don’t realize that a standard inheritance could actually harm their loved one by disqualifying them from crucial government benefits like Supplemental Security Income (SSI) and Medicaid.

A special needs trust solves this problem beautifully. This specialized legal tool allows you to improve your loved one’s quality of life without putting their essential benefits at risk. I’ve seen how these trusts bring families tremendous peace of mind.

What makes these trusts so valuable is their flexibility. Your special needs trust can provide for a wide range of life-enriching expenses that government benefits typically don’t cover. This might include educational opportunities that develop your loved one’s potential, specialized medical treatments not covered by Medicaid, or personal care attendants who provide compassionate support. The trust can also fund home furnishings and electronics that make daily life more comfortable, travel experiences that bring joy, and countless other quality-of-life improvements custom to your loved one’s unique interests and needs.

At Ironclad Law, we take a deeply personal approach to creating special needs trusts. We understand that each beneficiary has unique circumstances, preferences, and challenges. Our team works closely with you to design a trust that not only complies with all relevant regulations but also maximizes the benefits to your loved one in ways that matter most to them.

The peace of mind that comes from knowing your loved one will be cared for according to your wishes, even after you’re gone, is truly priceless. It’s why many of our clients tell us that setting up this trust was one of the most meaningful parts of their estate planning journey.

More info about special-needs planning

9. Protect Digital Assets & Passwords

Your online presence has become a significant part of your legacy. At Ironclad Law, we’ve noticed that estate planning needs now extend well beyond physical assets to include the digital footprint we all leave behind.

Think about it – your entire life might be stored in the cloud. From precious family photos to cryptocurrency investments worth thousands (or even millions), these digital assets need protection just like your home or bank accounts.

Your digital estate includes everything from the obvious (email accounts and social media profiles) to the potentially valuable (cryptocurrency wallets and online payment accounts). Don’t forget about digital photos, videos, domain names, websites, and even intellectual property you’ve created online. Even subscription services like Netflix or Spotify need consideration – someone may need to cancel these to avoid ongoing charges.

Creating a comprehensive digital asset inventory is the first step. We help our clients document where these assets exist and, most importantly, how to access them. This doesn’t necessarily mean writing down all your passwords (though secure password management is essential) – it means creating a legally sound plan for transferring digital access to your chosen representatives.

Many of our clients designate a specific “digital fiduciary” – someone tech-savvy who understands the value and sensitivity of your online presence. This person may be different from your primary executor if they have special knowledge of your digital holdings or technical expertise.

The legal landscape around digital assets continues to evolve. Many states, including ours, have adopted the Revised Uniform Fiduciary Access to Digital Assets Act (RUFADAA), which provides a framework for fiduciaries to legally access digital assets. Without proper planning, your loved ones might face unnecessary problems from service providers citing privacy policies – even when trying to access accounts of sentimental value.

For cryptocurrency holders, the stakes are particularly high. Without proper instructions, your Bitcoin or Ethereum could be permanently lost – we’ve seen entire fortunes disappear because no one knew how to access digital wallets after someone passed away.

At Ironclad Law, we make sure your estate planning needs include comprehensive digital asset protection that evolves as technology changes. Your online legacy deserves the same careful attention as everything else you’ve worked for.

10. Plan for Taxes & Lifetime Gifting

Let’s talk about something most folks would rather avoid thinking about – taxes. While it might not be the most exciting part of your estate planning needs, thoughtful tax planning can make a world of difference for your loved ones.

Currently, the federal estate tax exemption is quite generous at $13.61 million per person (2024), but here’s the kicker – it’s set to drop significantly after 2025, returning to around $5 million (adjusted for inflation). Plus, if you live in certain states, you might face state-level estate or inheritance taxes with much lower thresholds that could take a bite out of what you leave behind.

At Ironclad Law, we’ve seen how proactive tax planning creates breathing room for families. Annual exclusion gifts are one of our favorite strategies – you can give up to $18,000 per recipient in 2024 without touching your lifetime exemption. It’s a simple way to help children or grandchildren while reducing your taxable estate.

For married couples, we often discuss portability – essentially allowing spouses to combine their exemptions so the surviving spouse can use any unused portion of the deceased spouse’s exemption. This effectively doubles what you can shield from estate taxes.

Some families benefit from irrevocable life insurance trusts, which provide liquidity to pay estate taxes while keeping the insurance proceeds outside your taxable estate – a clever solution to ensure your heirs aren’t forced to sell assets just to pay the tax bill.

Charitable giving deserves special consideration too. Beyond the warm feeling of supporting causes you care about, charitable contributions reduce your taxable estate. We’ve helped clients establish charitable trusts that benefit both favorite charities and family members.

For clients with appreciating assets, we might recommend grantor retained annuity trusts (GRATs) – these specialized vehicles can pass future appreciation to your heirs with minimal gift tax impact.

Tax laws change frequently, which is why we work closely with our clients’ tax advisors to create flexible strategies. The goal isn’t just minimizing taxes – it’s making sure your hard-earned assets go where you want them to go, with as little friction as possible.

Good tax planning isn’t about avoiding your obligations – it’s about being smart with what you’ve built and ensuring your legacy benefits those you care about most.

11. Avoid Probate Where Possible

Let’s talk about probate – that court process most families would rather avoid if possible. I’ve seen countless clients breathe a sigh of relief when they learn there are legitimate ways to help assets bypass this often lengthy and expensive process.

Probate is simply the court’s way of overseeing the distribution of someone’s estate after they pass away. While it serves an important purpose, it comes with some significant drawbacks. It typically takes at least a year (sometimes several) to complete, can cost anywhere from 2-5% of your estate’s total value in fees, and perhaps most concerning for many families – it makes your personal financial information part of the public record.

At Ironclad Law, we help clients implement several effective probate-avoidance strategies:

Revocable living trusts work wonders for keeping assets out of probate. When you properly transfer ownership of your assets into your trust during your lifetime, those assets can pass directly to beneficiaries without court involvement. It’s like creating a private highway for your assets instead of forcing them through the public probate traffic jam.

Joint ownership with rights of survivorship offers another straightforward approach. When you co-own property this way, your share automatically transfers to the surviving owner when you pass away – no probate required. This works particularly well for married couples with shared assets.

Beneficiary designations are perhaps the simplest tool in our probate-avoidance toolkit. Your retirement accounts, life insurance policies, and bank accounts with payable-on-death (POD) or transfer-on-death (TOD) designations pass directly to named beneficiaries, completely bypassing probate.

For smaller estates, many states offer small estate procedures that significantly simplify the process. These streamlined options typically involve submitting an affidavit rather than going through full probate proceedings.

While some of these strategies are straightforward to implement, others require careful planning and proper legal documentation. The right approach depends entirely on your unique situation – your asset types, family dynamics, and long-term goals all factor into creating the most effective plan for your estate planning needs.

12. Updating Documents: The Evergreen Estate Planning Needs

Life doesn’t stand still, and neither should your estate plan. Think of your estate planning documents as living tools that need regular attention to stay effective. Even the most carefully crafted plan can become outdated as your life evolves and laws change.

At Ironclad Law, we often see clients who created a solid plan years ago but haven’t revisited it despite major life changes. Your estate planning needs shift with each significant milestone in your journey, and your documents should reflect your current reality—not your past circumstances.

When should you dust off those documents? Any major life event should trigger a review. Getting married or divorced dramatically changes your family structure and likely your wishes about who should inherit your assets. The birth of children or grandchildren might prompt you to add new beneficiaries or adjust how your assets will be distributed. Similarly, if someone named in your documents—like your chosen guardian for your children or the executor of your will—passes away, you’ll need to select someone new.

Financial changes matter too. Perhaps you’ve purchased a home, started a business, or received a substantial inheritance. These shifts in your asset portfolio often necessitate updates to your estate plan to ensure everything is properly protected and distributed according to your wishes.

Moving across state lines is another critical trigger for review. Estate laws vary significantly from state to state, and documents created in one jurisdiction might not work as intended in another. Your estate planning needs might include completely new documents that comply with your new home state’s requirements.

Even if none of these changes occur, we recommend following the five-year rule—reviewing your estate plan at least every five years to ensure it still aligns with your goals and complies with current laws. Tax laws, in particular, change frequently, and strategies that made sense under previous regulations might now be obsolete or even counterproductive.

At Ironclad Law, we understand that revisiting your estate plan might not be at the top of your to-do list. That’s why we’ve created maintenance programs that provide regular check-ins and updates, ensuring your plan continues to protect what matters most to you. These programs help catch potential issues before they become problems and give you the peace of mind that comes from knowing your affairs are in order.

An outdated estate plan can sometimes be worse than no plan at all, creating confusion and unintended consequences. Keeping your documents current isn’t just an administrative task—it’s an ongoing act of love and responsibility toward those you care about most.

Will vs. Trust: Choosing the Right Tool

“Should I get a will or a trust?” This is probably the most common question I hear when talking with clients about their estate planning needs. The truth is, there’s no one-size-fits-all answer. It really depends on your unique situation, what you’re trying to accomplish, and what matters most to you.

Let me break down the key differences in a way that hopefully makes your decision easier:

| Feature | Will | Revocable Living Trust |

|---|---|---|

| Probate | Required | Avoided for properly funded assets |

| Privacy | Becomes public record | Remains private |

| Effective | Only at death | During life and after death |

| Incapacity planning | None | Can provide for management during incapacity |

| Initial cost | Generally lower | Generally higher |

| Ongoing maintenance | Minimal | Requires funding and maintenance |

| Court oversight | Provided through probate | Limited unless disputes arise |

| Ease of challenging | Relatively easier | Generally more difficult |

Think of a will as your basic model car – it gets you where you need to go at a reasonable price. A will directs who gets what after you’re gone and names guardians for your children. It’s straightforward and costs less upfront. The downside? After you pass away, your family will need to go through probate court, which can be time-consuming, potentially expensive, and everything becomes public record – including what you owned and who got what.

A revocable living trust, on the other hand, is more like a luxury vehicle with extra features. Yes, it costs more initially, but it comes with significant benefits. Your assets can pass directly to your loved ones without court involvement. Everything stays private. And perhaps most importantly, a trust can protect you during your lifetime if you become incapacitated – something a will simply cannot do.

Many of our clients at Ironclad Law end up with both. We often create what we call a “belt and suspenders” approach – a revocable trust to handle most assets and avoid probate, paired with a simple “pour-over” will that catches anything you might have missed. This combination provides maximum protection and peace of mind.

I find that clients with straightforward situations and modest assets often do fine with just a will. But if privacy is important to you, you own property in multiple states, or you want protection during potential incapacity, a trust likely makes more sense.

The “right” choice isn’t about what works for most people – it’s about what works for your unique family situation, financial picture, and personal preferences. That’s why we always take the time to understand your specific estate planning needs before making any recommendations.

Beyond the Basics: Taxes, Probate, and Special Situations

While we’ve covered the fundamental estate planning needs that apply to most people, life is rarely one-size-fits-all. At Ironclad Law, we regularly help clients steer more complex planning scenarios that require specialized strategies and a deeper understanding of tax and probate implications.

State Estate and Inheritance Taxes

You might be surprised to learn that even if you’re well below the federal estate tax threshold, your estate could still face significant taxation at the state level. Twelve states plus the District of Columbia impose their own estate taxes with much lower exemption amounts than the federal government.

Even more confusing, six states collect inheritance taxes paid by beneficiaries rather than the estate itself, with tax rates that vary depending on your relationship to the deceased. If you live in Maryland, you face the double whammy of both taxes potentially applying to your estate.

For our New York clients, we pay particular attention to state estate tax planning since the exemption threshold is substantially lower than the federal one. We’ve seen cases where families who never imagined they’d face estate taxes ended up with significant state tax bills that could have been minimized with proper planning.

Blended Family Planning

If you’re in a second marriage with children from previous relationships, your estate planning needs become considerably more nuanced. Without thoughtful planning, you might unintentionally disinherit children from your first marriage or leave your current spouse with less than you intended.

We often recommend QTIP trusts for blended families, as they provide income to your surviving spouse while preserving the principal for your children from a previous marriage. Life insurance can also create immediate liquidity for certain beneficiaries without reducing what others receive. And those beneficiary designation forms we mentioned earlier? They become absolutely critical in blended family situations to prevent outdated designations from derailing your intentions.

Business Succession Planning

For business owners, your company isn’t just your livelihood—it’s often your most valuable asset and perhaps your legacy. A comprehensive succession plan ensures your business continues to thrive, provides for your family, and minimizes tax consequences when you’re no longer at the helm.

Buy-sell agreements establish a clear framework for ownership transition, while family limited partnerships or LLCs can facilitate the gradual transfer of business interests to the next generation. We often recommend life insurance as part of these plans to provide liquidity for buyouts or to equalize inheritances among heirs when only some are involved in the business.

Charitable Planning

If philanthropy matters to you, charitable planning can help you create a meaningful legacy while potentially providing tax benefits. Options range from simple charitable bequests in your will to more sophisticated strategies like charitable remainder trusts (which provide income to you or your beneficiaries for a period of time before the remainder goes to charity) or charitable lead trusts (which do the opposite).

Many of our clients find donor-advised funds particularly appealing as they offer immediate tax benefits while allowing ongoing influence over which charities receive grants from the fund. We’ve helped clients establish charitable legacies that will continue supporting their favorite causes for generations.

Medicaid Planning

The hard truth about aging is that long-term care costs can quickly deplete a lifetime of savings. With nursing home costs averaging over $100,000 annually in many areas, even substantial estates can be exhausted within a few years.

Medicaid planning strategies can help protect assets while ensuring access to needed care. Asset protection trusts, when established well in advance of need, can shield some assets from being counted for Medicaid eligibility purposes. Income-only trusts might allow you to qualify for benefits while preserving assets for your heirs. For married couples, we implement spousal protection strategies to ensure the well spouse isn’t impoverished by the ill spouse’s care needs.

Research published in scientific journals has shown that cognitive decline often begins earlier than most people realize, making advance planning for potential incapacity particularly important. According to studies highlighted by WebMD, subtle changes in financial decision-making ability can begin years before a clinical diagnosis of dementia.

At Ironclad Law, we take a compassionate approach to these difficult conversations, helping families prepare for potential care needs while protecting their hard-earned assets. Our experience with estate planning needs related to aging and incapacity allows us to provide practical guidance during emotionally challenging times.

More info about Medicaid strategies

Frequently Asked Questions about Estate Planning Needs

What happens if I die without a will?

The thought of leaving your loved ones without clear instructions is something none of us wants to consider. Yet nearly half of American adults haven’t taken this crucial step.

If you pass away without a will (legally termed “intestate”), your state steps in and makes all the decisions for you. Your assets follow a predetermined path based on your state’s intestacy laws, which typically flow through a family tree hierarchy: first to spouse, then children, parents, siblings, and eventually more distant relatives.

In New York, for example, if you’re married with children, your spouse receives the first $50,000 plus half of your remaining estate, with your children dividing the other half. This arrangement might work for some families, but could create serious problems in blended families or when minor children are involved.

Without a will, the court also appoints an administrator (someone you didn’t choose) to manage your estate. This typically extends the probate process, adding months of delay and thousands in additional costs your family must bear. Most painfully, if you have minor children, a judge – not you – decides who will raise them.

How often should I review my plan?

Life doesn’t stand still, and neither should your estate plan. At Ironclad Law, we’ve seen too many outdated plans fail families when they needed protection most.

Your estate planning needs evolve with your life. I recommend reviewing your documents after any major life milestone – marriages, divorces, births, deaths, or significant financial changes. Moving to a different state also necessitates a review, as estate laws vary dramatically across state lines.

Even without these triggers, dust off your estate plan at least every five years. Tax laws change, family dynamics shift, and your own wishes may evolve in ways you hadn’t anticipated.

Financial powers of attorney deserve special attention – many banks and investment companies have become increasingly reluctant to honor documents older than five years, even when legally valid. Keeping these current prevents headaches for your loved ones during already difficult times.

Do I really need an attorney?

In our digital age, DIY estate planning websites promise quick, inexpensive solutions. While tempting, these one-size-fits-all approaches often create more problems than they solve.

Think of it this way: would you perform your own surgery to save money? Your estate planning needs deserve professional attention, especially if your situation involves any complexity at all.

Online templates simply can’t address the nuances of:

- Blended families with children from multiple relationships

- Business ownership and succession planning

- Special needs dependents requiring lifetime support

- Multi-state property ownership

- Substantial assets requiring tax planning

- Asset protection concerns

- Complex beneficiary situations

At Ironclad Law, we’ve unfortunately had to help many families clean up problems created by inadequate DIY documents – often at much greater expense than proper planning would have cost initially. Our attorneys take time to understand your unique situation, creating personalized solutions that truly protect what matters most to you.

The peace of mind that comes from knowing your plan will actually work when your family needs it most is invaluable. Your loved ones deserve that security, and you deserve that confidence.

Lawyers Specializing in Wills and Trusts Near Me

Conclusion

Planning for your future isn’t something any of us particularly enjoy thinking about. Yet addressing your estate planning needs is one of the most caring things you can do for yourself and the people you love. It’s not just about what happens after you’re gone—it’s about protecting what matters throughout your entire life journey.

A thoughtful estate plan gives you control when you need it most. If you become ill or injured, your healthcare directives ensure medical decisions reflect your wishes. If you’re temporarily unable to manage your finances, your power of attorney keeps things running smoothly. And yes, when you eventually pass away, your carefully crafted plan provides for your loved ones exactly as you intended.

At Ironclad Law, we see the relief on clients’ faces once their plans are in place. That weight lifting off their shoulders tells us everything we need to know about the value of proper planning. We understand that diving into these waters can feel overwhelming at first—that’s completely normal. That’s why we take a personal approach, walking beside you through each step and focusing on what matters most to your unique situation.

Our attorneys bring both expertise and genuine compassion to the table. We’ll explain everything in plain English (no confusing legalese), answer all your questions, and create documents that truly reflect your wishes. We believe peace of mind shouldn’t be complicated.

Don’t leave your legacy to chance or put this off for “someday.” Your future self and your loved ones will thank you for taking action today. Contact Ironclad Law to schedule a friendly, no-pressure consultation about your estate planning needs. Our experienced New York estate planning team is ready to help you protect what matters most to you.