You have 0 items in your cart

Why Business Insolvency Advice Can Save Your Company

Business insolvency advice is the difference between closing your doors forever and finding a path forward when your company can’t pay its debts. When creditors are calling, cash flow has dried up, and you’re facing the possibility of losing everything you’ve built, the right guidance can turn a crisis into a comeback.

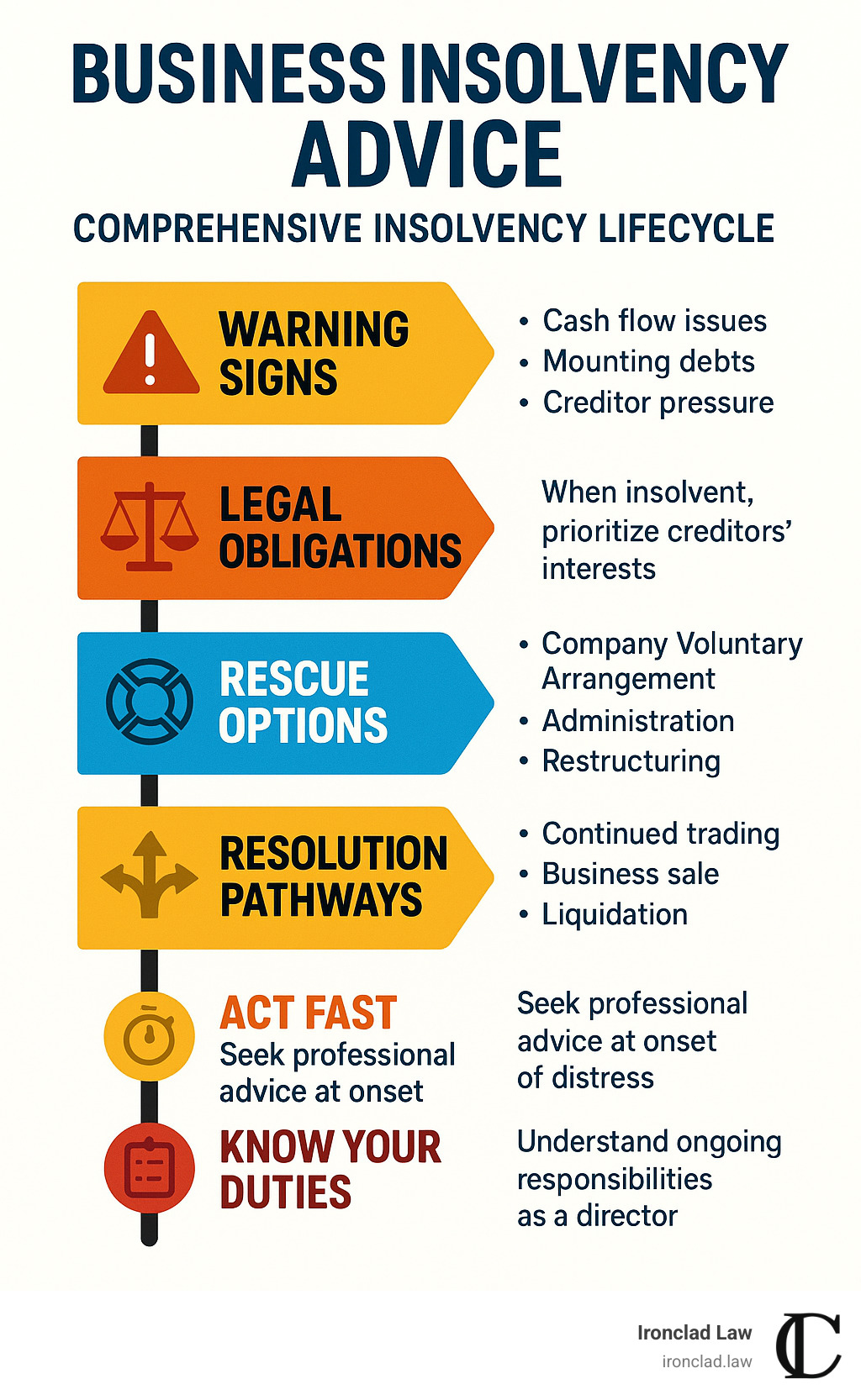

Essential Business Insolvency Advice at a Glance:

- Act Fast: Contact a Licensed Insolvency Trustee or Insolvency Practitioner immediately when warning signs appear

- Know Your Options: Restructuring, administration, voluntary arrangements, or liquidation each serve different situations

- Understand Director Duties: You must prioritize creditors’ interests once insolvency threatens to avoid personal liability

- Communicate Openly: Creditors are more likely to negotiate when they see proactive management

- Explore Rescue Routes: Company Voluntary Arrangements (CVAs), administration, and informal workouts can preserve your business

Business insolvencies in Canada increased by more than 41% in 2023, while the UK saw 5,595 businesses enter insolvency in Q3 2022 alone – a 40% jump from the previous year. Many of these situations could have been prevented or resolved differently with early, expert intervention.

The key is understanding that insolvency isn’t bankruptcy – it’s a financial state that, with proper guidance, doesn’t have to mean the end of your business. Whether you’re dealing with cash flow problems, mounting debt, or creditor pressure, there are legal frameworks designed to help viable businesses survive and thrive.

I’m Michael Hurckes, Managing Partner at Ironclad Law, where I’ve spent years helping business owners steer complex financial and legal challenges through aggressive representation and strategic counsel. My experience in corporate law, regulatory compliance, and business insolvency advice has shown me that the right legal strategy at the right time can mean the difference between business failure and financial recovery.

Business insolvency advice terms explained:

– business contract management

– business dispute resolution

– business entity formation

Spot the Storm: Early Warning Signs of Insolvency

Business insolvency advice is like weather forecasting – the earlier you spot the storm clouds, the better your chances of finding shelter. Insolvency happens when your business can’t pay its bills as they come due, or when what you owe is more than what you own.

Business insolvencies jumped 41% in Canada during 2023, while the UK saw 5,595 companies enter insolvency in just one quarter. Behind each statistic is a business owner who missed the warning signs or waited too long to act.

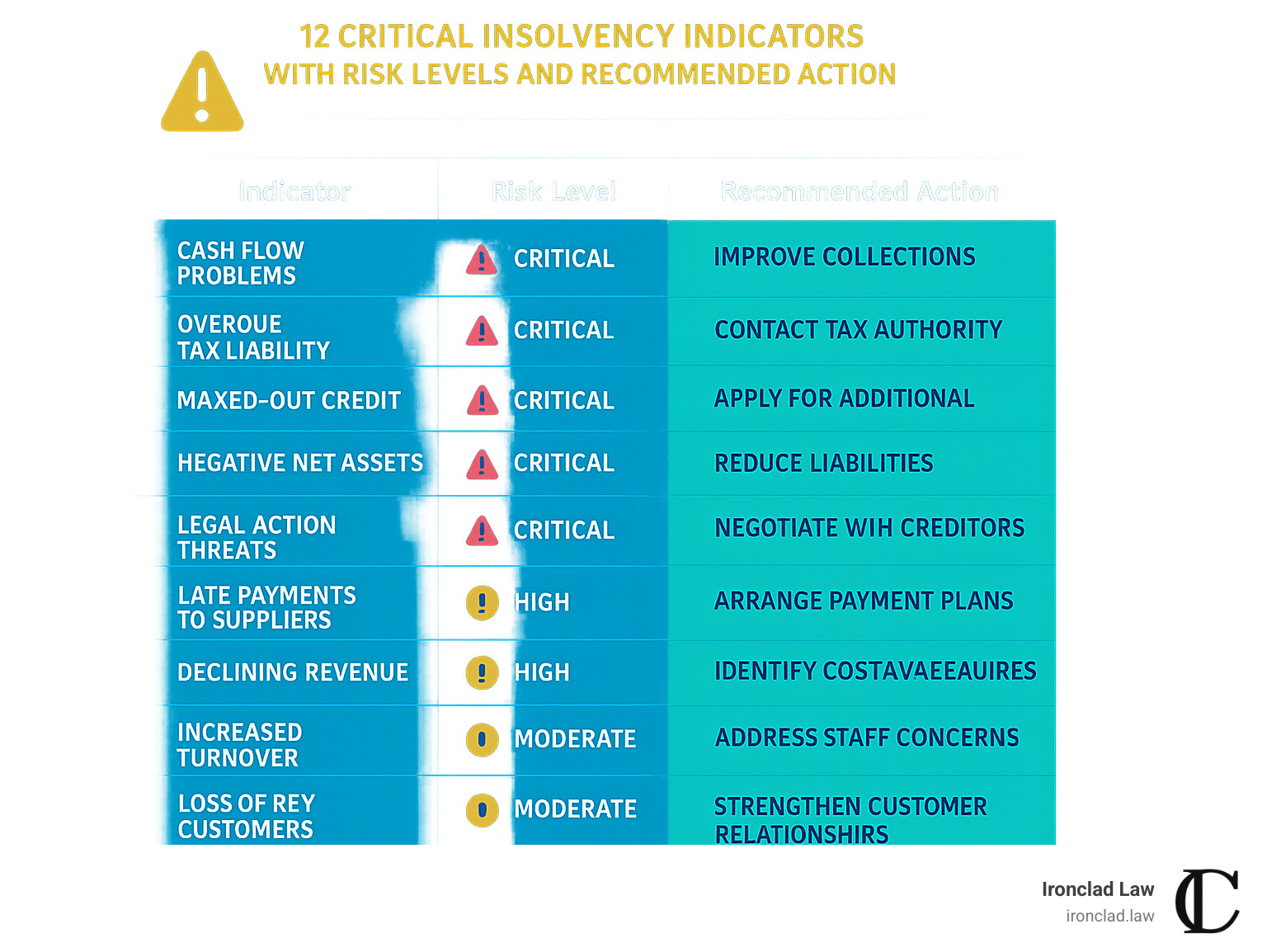

Key Financial Red Flags

Cash flow gaps become your biggest enemy when you’re constantly borrowing just to cover basics like payroll and rent. When you’re robbing Peter to pay Paul every month, you’ve crossed into dangerous territory.

Overdue tax payments should trigger immediate action. Tax authorities have powers that would make your other creditors jealous – they can freeze accounts, seize assets, and shut you down faster than you can blink. The UK’s HMRC Time to Pay arrangements can provide breathing room, but only if you reach out before they come knocking.

Maxed out credit lines signal that traditional lenders have lost faith in your ability to repay. When banks start saying no and your business credit cards hit their limits, you’ve lost crucial financial flexibility.

Balance sheet insolvency occurs when your debts exceed your assets on paper. Even if you’re still paying bills today, this mathematical reality means you’re technically insolvent and need professional help immediately.

Operational Symptoms

Mounting creditor pressure escalates quickly from friendly reminders to legal threats. When suppliers demand cash on delivery and lawyers’ letters fill your mailbox, you’re in the danger zone.

Staff turnover accelerates when employees sense trouble. Good people jump ship first, leaving you with a weakened team right when you need all hands on deck.

Supplier holdbacks create a domino effect. When key suppliers put you on credit hold or demand payment upfront, your ability to deliver to customers gets compromised.

Creditors are more willing to negotiate when they see you actively trying to minimize losses. Early action isn’t just about survival – it’s about keeping your negotiating power and credibility intact.

Know Your Legal Duties & Director Liabilities

When your company faces financial trouble, you’re navigating a legal minefield where one wrong step could make you personally responsible for company debts. The moment your company can’t pay its bills, your primary duty shifts from serving shareholders to protecting creditors.

Insolvency vs Bankruptcy: Core Distinctions

Insolvency is your financial condition – it means your business either can’t pay its debts when they’re due or owes more than it owns. Bankruptcy is a legal process – it’s what happens when you or a court decides to formally deal with insolvency through official proceedings.

The balance sheet test looks at your assets versus liabilities on paper. The cash flow test is more immediate: can you pay your bills this month? You could pass one test and fail the other, but failing both means you need business insolvency advice immediately.

Personal Exposure & Safe Harbour

Wrongful trading can make you personally liable for company debts if you keep operating when you know (or should reasonably know) the business is insolvent. The “should reasonably know” part is crucial – ignorance isn’t a defense if warning signs were obvious.

Personal guarantees you signed years ago don’t disappear just because the company goes under. Banks and landlords particularly love these guarantees because they provide a backup plan.

Directors and Officers (D&O) liability extends beyond financial decisions. You can face personal liability for unpaid payroll taxes, employee wages under wage protection schemes, and various statutory obligations.

Criminal sanctions can apply in cases of fraudulent trading, failure to keep proper records, or other misconduct. Consequences can include disqualification from being a director and even prison time.

The good news is that “safe harbour” protections exist for directors who act responsibly. Getting professional business insolvency advice early and following it demonstrates that you’re trying to minimize losses and act in creditors’ best interests.

Only licensed professionals from recognized professional bodies can act as insolvency practitioners.

For comprehensive guidance on protecting yourself and your business, our Legal Risk Management services can help you understand and mitigate director liabilities while you still have options.

Early action protects you legally and financially. The longer you wait to address insolvency issues, the fewer protections you’ll have and the greater your personal exposure becomes.

Business Insolvency Advice: Rescue & Resolution Toolbox

Business insolvency advice is your emergency toolkit – different situations call for different tools. When your company hits financial trouble, you’re not automatically doomed to close your doors. The legal system offers several lifelines, from gentle restructuring to controlled liquidation.

Business Insolvency Advice for Restructuring

Company Voluntary Arrangements (CVAs) are like negotiating a payment plan with all your creditors at once. Your business keeps running while you pay back reduced amounts over time. You need at least 75% of your creditors by value to agree to your proposal.

CVAs work when your business model still functions but cash flow has gone sideways. If you can show creditors a realistic path back to profitability, they often prefer getting something over several years rather than pennies on the dollar through liquidation.

Informal workouts happen before you involve lawyers and courts. You contact your biggest creditors directly to negotiate extended payment terms or partial payments.

Debtor-in-Possession (DIP) financing allows new lenders to get super-priority status – they get paid first, even before existing creditors. This makes banks willing to lend during restructuring, giving you working capital to turn things around.

HMRC Time to Pay arrangements offer specific relief for UK businesses struggling with tax debt. The tax authority would rather collect something than nothing, so they’ll often negotiate payment plans if you approach them proactively.

Business Insolvency Advice for Administration & Receivership

Administration puts your business in intensive care. A licensed insolvency practitioner takes control from directors and gets automatic protection from creditors while they work on a rescue plan.

Receivership happens when a secured creditor (usually your bank) calls in the loans. They appoint a receiver to recover what they’re owed from assets they hold security over.

Business Insolvency Advice for Liquidation

Creditors’ Voluntary Liquidation (CVL) lets you control the process rather than having it forced on you. Of the 5,595 UK businesses that entered insolvency in Q3 2022, 86% chose CVL.

Members’ Voluntary Liquidation (MVL) is for solvent businesses whose owners want to wind up anyway. Compulsory liquidation happens when creditors petition the court to shut you down – expensive, public, and completely out of your control.

| Liquidation Type | Who Controls | Best For | Timeline |

|---|---|---|---|

| CVL | Directors initially, then liquidator | Insolvent companies seeking orderly closure | 6-18 months |

| MVL | Members/shareholders | Solvent companies with surplus assets | 3-12 months |

| Compulsory | Court-appointed liquidator | Creditor-driven when other options fail | 12-24 months |

Our Business Dispute Resolution services help steer the complex negotiations that surround these processes.

Immediate Action Plan & Prevention Strategies

When the warning signs start flashing, you don’t have the luxury of time. The businesses that survive insolvency crises are the ones that move fast and move smart in those critical first hours.

48-Hour Survival Checklist

The first six hours are about stopping the bleeding. Stop all non-essential spending immediately – cancel that marketing campaign, postpone equipment purchases, and halt any discretionary spending.

Next, create a cash flow snapshot that shows exactly how much money you have right now and when your major payments are due. How much is in your accounts? What bills are due this week? Which creditors are likely to take action first?

Cease any activities that could constitute wrongful trading right away. Once you know your company is insolvent, continuing to trade can make you personally liable for company debts.

Within 24 hours, you need professional help. Contact a Licensed Insolvency Trustee or Insolvency Practitioner for an emergency consultation. Most experienced practitioners understand that insolvency crises don’t follow business hours.

Prepare a comprehensive creditor list with exact amounts owed and payment terms. Draft board minutes documenting the financial situation and decisions you’re making. This paper trail becomes crucial if anyone later questions whether you acted responsibly.

The second day is about building your strategy. Start implementing immediate cost-cutting measures while beginning creditor communications to buy time and show you’re acting in good faith.

Long-Term Insolvency Prevention

Build early warning systems that track your key financial ratios, cash flow trends, and operational metrics. Set up monthly reviews of your liquidity ratios, monitor how long customers are taking to pay, and watch for increases in staff turnover.

Diversification isn’t just investment advice – it’s survival strategy. Over-reliance on single customers, suppliers, or revenue streams creates dangerous vulnerability.

Stay on top of compliance, especially tax obligations. Falling behind on payroll taxes or VAT payments can push a struggling business over the edge into insolvency.

Develop scenario plans for different economic conditions. What would you do if your biggest customer stopped paying? How would you handle a 30% drop in revenue?

Build professional relationships before you need them. Establish connections with insolvency practitioners and business advisors while times are good.

For businesses looking to build robust operational frameworks that prevent insolvency, our Strategic Business Planning services help create sustainable business models with built-in risk management.

The Business debt resources from official government sources provide additional guidance on managing business financial obligations before they become critical.

Frequently Asked Questions about Business Insolvency Advice

What does a Licensed Insolvency Trustee or Insolvency Practitioner actually do?

Think of a Licensed Insolvency Trustee or Insolvency Practitioner as a financial emergency room doctor for your business. They’re highly specialized professionals who’ve undergone years of rigorous training specifically for these situations.

A Licensed Insolvency Trustee is an officer of the Court regulated by the Office of the Superintendent of Bankruptcy who acts as an officer of the court, applying both accounting and legal expertise for the benefit of all stakeholders. This means they have a legal duty to be fair to everyone involved.

Their assessment role is crucial. They’ll determine whether your business can realistically be saved or if it’s time to close the doors. When administering formal procedures like CVAs, administration, or liquidation, they take control of the process so you don’t have to steer complex legal requirements while dealing with financial crisis.

Insolvency practitioners have duties to investigate director conduct. They’re required to report any misconduct to authorities, but they’re also there to protect directors who’ve acted properly.

How long and how much will insolvency proceedings cost?

Timeline expectations vary significantly by procedure. Proposals and CVAs typically take 2-5 years to complete. Administration usually runs 6-18 months. Bankruptcy generally lasts 2 years, while liquidation can take anywhere from 6-24 months.

Cost-wise, you’re looking at $7,500-$25,000 plus disbursements for bankruptcy, $15,000-$50,000 plus disbursements for proposals, and varying amounts for CVAs.

These costs are usually far less than what you’ll lose by not taking action. Most business insolvency advice professionals offer initial consultations at no charge and will structure payments over time to help with cash flow.

How can open communication with creditors improve outcomes?

Your creditors often want to help you succeed. Creditors are more likely to agree to repayment plans when they see a company actively minimizing losses.

Proactive communication is your secret weapon. Instead of avoiding creditors’ calls, reach out before they have to chase you. Regular updates matter enormously, even when you don’t have good news.

Creditors are business people who understand that recovering 70% of a debt through negotiation beats recovering 20% through liquidation. When you approach them professionally with a realistic plan, you’re often surprised by their willingness to work with you.

Conclusion

When you’re staring at unpaid bills and wondering if you’ll have to close the doors on everything you’ve built, it’s easy to think that business insolvency advice is just about managing the inevitable end. But that’s not the whole story.

Those statistics we discussed – the 41% spike in Canadian business insolvencies and the 5,595 UK companies that entered formal proceedings – don’t show the companies that turned things around. The businesses that used CVAs to restructure their debts and came back stronger. The directors who protected themselves from personal liability by acting quickly.

Financial distress doesn’t have to be a death sentence for your business. With the right approach, it can be a turning point.

The businesses that make it through these challenges share common traits. They act quickly instead of hoping things will magically improve. They communicate honestly with creditors instead of hiding. They get professional help early instead of trying to figure it out alone. Most importantly, they treat insolvency as a problem to solve, not a failure to hide from.

At Ironclad Law, we’ve seen how the right legal strategy can change everything. Our assertive approach means we don’t just file paperwork and hope for the best. We fight for our clients’ interests – whether that’s negotiating with tough creditors, defending against personal liability claims, or structuring deals that save jobs and preserve business value.

We understand that behind every balance sheet is a person who’s put their heart, soul, and probably their life savings into building something meaningful. That’s why our approach in Florida and New York has always been about aggressive representation combined with practical business sense.

Insolvency is a financial state, not a final judgment. Companies recover from it every day. Directors protect themselves and their families from personal ruin. Creditors get paid more than they expected. It happens more often than the headlines suggest, and it can happen for you too.

But only if you act. Only if you get the right guidance. Only if you treat this challenge as something to be solved, not something to be endured.

If you’re seeing the warning signs we’ve discussed, or if creditors are already breathing down your neck, don’t spend another sleepless night wondering what comes next. The sooner you understand your options, the more options you’ll have.

Ready to turn this crisis into your comeback story? Schedule a Business Lawyer Consultation with our team today.