You have 0 items in your cart

Understanding Securities Licensing Requirements

Thinking about starting a career in financial services? Let’s talk about two critical licenses you’ll likely need: Series 6 and Series 63. These aren’t just random numbers and paperwork—they’re your ticket to helping clients build their financial futures!

I’ve guided countless professionals through this licensing maze, and I’m here to break it down in plain English. Here’s what you need to know about these two essential credentials:

| License | Purpose | Administrator | Questions | Time | Pass Score | Cost |

|---|---|---|---|---|---|---|

| Series 6 | Allows sales of packaged securities (mutual funds, variable annuities) | FINRA | 50 | 90 min | 70% | $75 |

| Series 63 | Permits securities sales across state lines (Blue Sky law compliance) | NASAA/FINRA | 60 | 75 min | 72% | $147 |

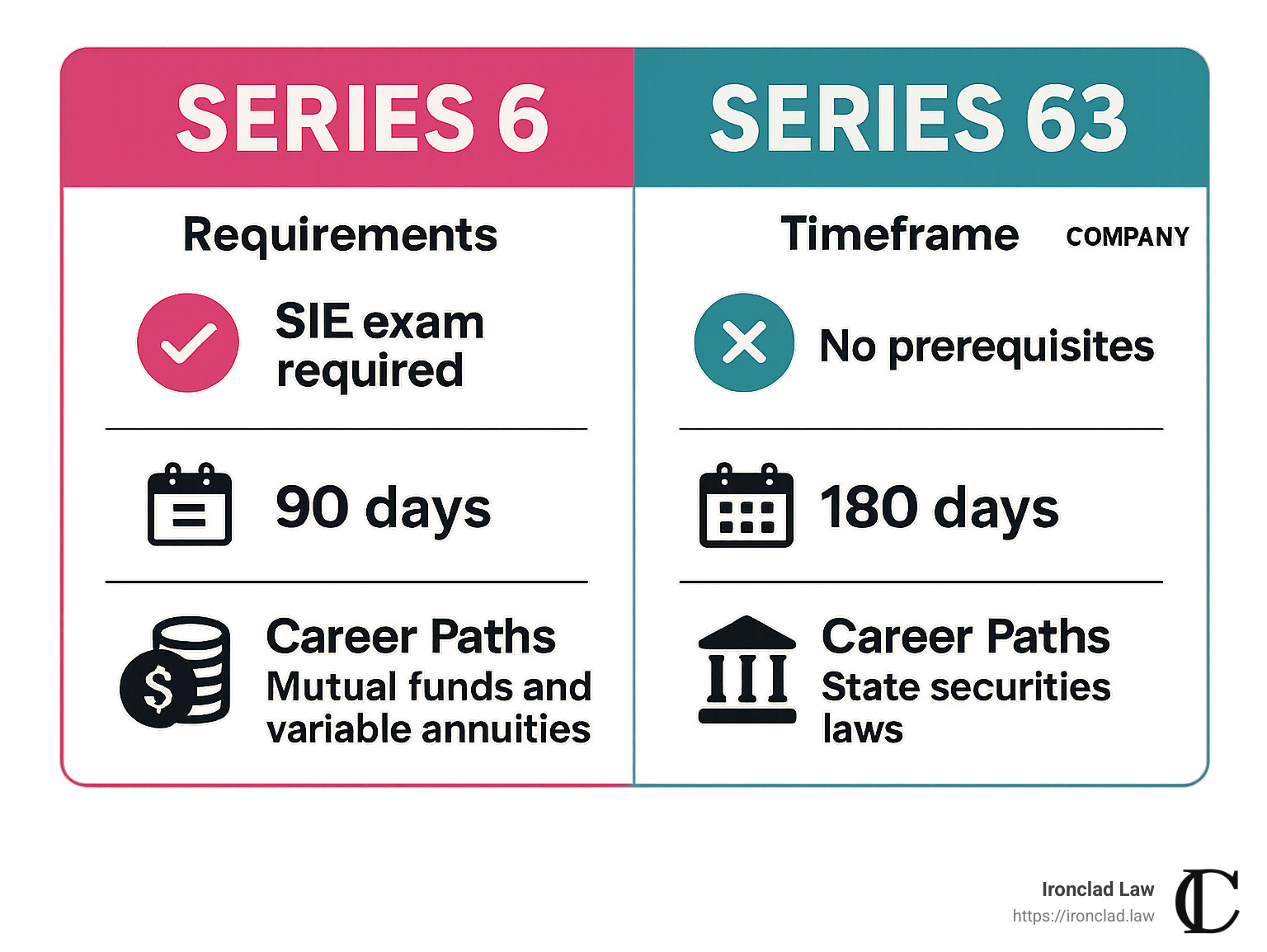

Think of the Series 6 license as your passport to selling packaged investment products. Its official name is quite a mouthful—the Investment Company and Variable Contracts Products Representative Qualification Exam—but its purpose is straightforward. With this license, you can help clients invest in mutual funds, variable annuities, and variable life insurance products. One important note: you’ll need to pass the Securities Industry Essentials (SIE) exam first before tackling the Series 6.

The Series 63 license (Uniform Securities Agent State Law Examination) is all about understanding state securities regulations—often called “Blue Sky laws” because they aim to protect investors from offers that have “nothing but blue sky” behind them. Most states require this license, though there are exceptions: Colorado, Florida, Louisiana, Maryland, New Jersey, Ohio, Vermont, and the District of Columbia have waived this requirement.

When comparing these licenses, remember:

Series 6 focuses specifically on packaged investment products, limiting what you can sell but providing a more focused exam. Series 63, on the other hand, covers state-specific securities laws and applies to a broader range of securities sales. While the Series 6 requires completing the SIE first, the Series 63 has no prerequisites.

Here’s the reality: most financial professionals need both licenses to work effectively across state lines and provide a useful range of investment options to their clients. Think of them as complementary tools in your professional toolkit.

I’m Michael Hurckes, Managing Partner at Ironclad Law, and I’ve spent years helping professionals steer FINRA regulations and licensing requirements. Whether you’re just starting out or looking to expand your securities practice, understanding these licenses is crucial to building a compliant and successful career.

Looking for more information about Series 6 and Series 63 and other securities licensing requirements? Check out these helpful resources:

– Securities license exam details and preparation tips

– Series 7 exam requirements for those considering broader securities licensing

– SIE exam information for your essential first step

1. Why Get Licensed? The Value Proposition

Let’s talk about why these licenses matter in the real world. I’ve seen countless financial professionals transform their careers after getting their Series 6 and Series 63 licenses—and it’s not just about following rules.

Think about it from your clients’ perspective. When you hand them your business card with those credentials, you’re not just showing a piece of paper. You’re demonstrating your commitment to mastering your craft. Clients immediately feel more at ease knowing you’ve proven your knowledge through rigorous testing.

One advisor I know put it perfectly: “Before my licenses, prospects would hesitate. After getting licensed, those same prospects started calling me for advice. The licenses didn’t change what I knew—they changed how people perceived what I knew.”

Beyond building trust, these licenses are non-negotiable for compliance. Without them, you simply can’t legally sell certain investment products or work across state lines. Your firm risks hefty fines, and you risk your entire career. The financial industry takes these requirements seriously, and so should you.

Series 6 Benefits: Product Sales Power

The Series 6 license opens doors to selling what we call “packaged investment products.” This might sound limiting compared to the broader Series 7, but these products represent the backbone of what most everyday investors actually need.

With your Series 6, you can confidently offer:

Mutual funds that give your clients diversified exposure to markets without needing to pick individual stocks. Whether it’s growth funds for younger clients or income funds for retirees, you’ll have tools for every situation.

Variable annuities that combine insurance protection with investment opportunity—perfect for clients concerned about both growth and guarantees.

Variable life insurance policies that offer death benefits while allowing policyholders to build potential investment value.

Municipal fund securities including 529 college savings plans that help families prepare for educational expenses.

For many financial professionals, especially those coming from insurance backgrounds, the Series 6 provides the perfect complement to their existing expertise. You can seamlessly transition from discussing protection needs to building wealth—all within your licensing authority.

Series 63 Benefits: Crossing State Lines

While your Series 6 determines what you can sell, your Series 63 determines where you can sell it. This license reflects your understanding of state securities regulations—often called “Blue Sky Laws.”

The colorful “Blue Sky” nickname has a fascinating origin. Back in the early 1900s, a Kansas judge described fraudulent securities as having “no more basis than so many feet of blue sky.” The name stuck, and these state-level investor protection laws have been known as Blue Sky Laws ever since.

With your Series 63, you’ll demonstrate proficiency in:

State registration requirements for both securities products and the professionals who sell them.

Fiduciary duties and ethical standards that put client interests first—something today’s investors value tremendously.

Fraud prevention protocols that protect both your clients and your practice.

The practical benefit? Freedom to serve clients regardless of where they live. Without a Series 63, state borders become business barriers. Imagine having to turn away a valued client simply because they moved to another state—or missing opportunities with referrals who live across state lines.

One advisor told me: “My Series 63 paid for itself the first month when a client’s daughter in another state needed help with her inheritance. Without it, I would have had to refer her elsewhere.”

Even if you primarily work in one state today, the Series 63 gives you flexibility as your practice grows and evolves.

2. Who Oversees the Exams & Who Can Sit?

Ever wonder who’s behind those nerve-wracking financial exams? Understanding the regulatory landscape helps make sense of why these licenses matter so much in the industry. The Series 6 and Series 63 exams have different “parents,” though they’re often taken as a pair.

The Series 6 is developed and maintained by FINRA (Financial Industry Regulatory Authority), the watchdog organization that oversees all broker-dealers in the United States. They’re the ones who create the questions, determine what constitutes a passing grade, and regularly update the content to keep pace with changing regulations.

On the other hand, the Series 63 is created by NASAA (North American Securities Administrators Association), the organization representing state securities regulators. While NASAA develops the exam, FINRA actually administers it on their behalf—think of it as NASAA writing the test, but FINRA proctoring it.

Both exams take place at Prometric testing centers across the country, where you’ll find standardized conditions and those lovely security protocols we all enjoy (hello, locker storage and palm scans!).

So who can actually sit for these exams? The requirements differ slightly:

For the Series 6, you’ll need to:

– First pass the Securities Industry Essentials (SIE) exam—this is non-negotiable

– Have sponsorship from a FINRA member firm (your employer)

– Have your Form U4 (the industry registration application) filed by your sponsoring firm

– Complete fingerprinting and background checks (yes, they’ll know about that parking ticket)

For the Series 63, things are a bit more flexible:

– No prerequisites or other exams required first

– No firm sponsorship technically required (you can take it as a self-study candidate)

– Registration through FINRA’s Central Registration Depository (CRD)

While you can technically take the Series 63 without being sponsored by a firm, most professionals take it while employed since they’ll need both licenses to actually conduct business. As one advisor told me, “I took my 63 before I had a job offer, thinking it would make me more marketable. In retrospect, I should’ve waited since my firm would have paid for it!”

Eligibility Checklist for Series 6 and Series 63

Before you register, make sure you tick all these boxes:

✓ Age requirement: At least 18 years old (sorry, teen prodigies)

✓ SIE exam: Passed for Series 6 (not needed for Series 63)

✓ Firm sponsorship: Required for Series 6, optional for Series 63

✓ Form U4 filing: Completed by your sponsoring firm

✓ Fingerprinting: Required for FINRA registration

✓ Background check: Covers criminal history, financial disclosures, and regulatory actions

✓ Exam fees paid: $75 for Series 6, $147 for Series 63

One cool program worth knowing about is the Exam Validity Extension Program (EVEP). This NASAA-approved initiative allows eligible individuals to keep their Series 63 exam results valid for up to five years by completing annual continuing education—even if they’re not currently working with a firm. It’s perfect if you’re taking a career break but plan to return to the industry.

States That Waive Series 63

Not all states require the Series 63, which is a nice break if you happen to work in one of these jurisdictions:

- Colorado

- Florida

- Louisiana

- Maryland

- New Jersey

- Ohio

- Vermont

- District of Columbia

But here’s the reality check: even if you’re based in one of these states, you’ll likely still need the Series 63 if you have clients in other states or if your firm requires it as standard policy. Most national firms make all their representatives get the Series 63 regardless of home state—it ensures you can help clients wherever they might move.

As one veteran advisor with 25 years of experience put it: “I’ve never met a successful advisor who regretted getting their Series 63, even when they started in a state that didn’t require it. But I’ve met plenty who regretted not having it when a million-dollar client moved to a state where it was required.”

3. Exam Mechanics at a Glance

Tackling the Series 6 and Series 63 exams feels less daunting when you understand what you’re walking into. Let’s break down exactly what to expect when you sit for these tests.

Here’s a side-by-side comparison that shows you the key differences:

| Feature | Series 6 | Series 63 |

|---|---|---|

| Total questions | 55 (50 scored, 5 unscored) | 65 (60 scored, 5 unscored) |

| Time limit | 90 minutes | 75 minutes |

| Passing score | 70% (35 out of 50) | 72% (43 out of 60) |

| Question format | Multiple-choice | Multiple-choice |

| Test location | Prometric centers | Prometric centers |

| Unscored items | 5 pretest questions | 5 pretest questions |

| Retake waiting period | 30 days after 1st failure; 30 days after 2nd; 180 days after 3rd | 30 days after 1st failure; 30 days after 2nd; 180 days after 3rd |

| Exam fee | $75 | $147 |

| Exam window | 120 days after enrollment | 120 days after enrollment |

Both exams sprinkle in those sneaky unscored “pretest” questions that look identical to the real ones. These are essentially questions FINRA and NASAA are test-driving for future exams. Since there’s no way to tell which questions are which, your best strategy is to treat every question like it counts.

If you’re wondering about the Series 6 structure, it got a makeover in October 2018. Now you need to pass the Securities Industry Essentials (SIE) exam first, before tackling the Series 6 “top-off” exam. This change wasn’t just bureaucratic shuffling—it was part of FINRA’s effort to create a common foundation across different securities licenses.

Series 6 and Series 63: Content Breakdown

These two exams are testing completely different knowledge bases, which makes sense given their distinct purposes.

The Series 6 exam organizes content around four job functions that mirror what you’d actually do in the field:

-

Seeks Business for the Broker-Dealer (24% of exam) covers the regulatory requirements you need to know, different types of securities and accounts, and the tax implications that might affect your clients’ decisions.

-

Opens Accounts After Obtaining and Evaluating Customers’ Financial Profile and Investment Objectives (16% of exam) digs into different account types, how to assess client suitability, and the paperwork needed to open accounts properly.

-

Provides Customers with Information About Investments, Makes Recommendations, Transfers Assets and Maintains Appropriate Records (50% of exam) forms the heart of the exam, covering product details, how to make appropriate recommendations, and the mechanics of trading.

-

Obtains and Verifies Customers’ Purchase and Sales Instructions; Processes, Completes and Confirms Transactions (10% of exam) tests your knowledge of order execution, confirmation procedures, and record-keeping requirements.

The Series 63 exam, meanwhile, focuses on four regulatory areas:

-

Regulation of Investment Advisers, Broker-Dealers, and Agents (45% of exam) covers who needs to register where, what records you need to keep, and ongoing requirements after registration.

-

Registration of Securities (10% of exam) examines when securities need to be registered and when they might be exempt.

-

Business Practices, Customer Communication, and Ethical Considerations (20% of exam) tests your knowledge of proper client communications, disclosure requirements, and your ethical obligations.

-

Remedies and Administrative Provisions (25% of exam) covers what happens when things go wrong—administrative actions, civil liabilities, and remedies available to investors.

Series 6 Focus Areas

When studying for the Series 6, you’ll need to become comfortable with the nuts and bolts of packaged investment products.

The exam places heavy emphasis on Customer Accounts—you’ll need to understand the difference between individual, joint, trust, and corporate registrations, plus all the transfer procedures and documentation requirements.

You’ll also need deep knowledge of Product Information, including all the features, risks, and tax implications of mutual funds, variable annuities, variable life insurance, and municipal fund securities. This isn’t just theoretical—clients will ask you these questions daily.

The exam also tests Opening Transactions, including proper account opening procedures, suitability requirements, and your obligation to really know your customer before making recommendations.

Finally, Suitability is a critical focus area. You need to demonstrate that you can match investment recommendations to your clients’ unique financial situations, objectives, risk tolerance, and time horizons. This isn’t just about passing an exam—it’s about developing the judgment that will protect both your clients and your career.

Series 63 Focus Areas

The Series 63 exam is all about state securities laws and ensuring you don’t accidentally break them.

A huge portion focuses on Registration of Persons—who needs to register in each state, who might be exempt, and the entire registration process for broker-dealers, agents, investment advisers, and investment adviser representatives. This is the nuts-and-bolts knowledge that keeps you on the right side of regulators.

You’ll also need to understand Securities Registration requirements in different states, including when securities need to be registered and when they might qualify for exemptions. Selling unregistered, non-exempt securities can lead to serious consequences, so this knowledge is critical.

The exam also tests your understanding of proper Business Practices, including your ethical obligations, prohibited conduct, required disclosures, and fiduciary responsibilities. These questions often present ethical dilemmas that test your judgment.

Finally, Fraud Prevention is a key area, covering how to identify and prevent securities fraud, material misrepresentations, and omissions. Regulators take fraud very seriously, and they expect you to be their first line of defense.

Research from the American Psychological Association suggests that understanding test structure and content actually improves performance. When you know what topics will be tested, you can study more efficiently and retain information better—which is exactly why we’ve broken down these exams in such detail.

Scientific research on test-taking strategies

4. Registering, Scheduling & Passing on the First Try

Ready to take your Series 6 and Series 63 exams? The registration process is straightforward, but there are a few key differences between these two tests that you’ll want to know about.

For the Series 6, you’ll need to:

1. Pass the Securities Industry Essentials (SIE) exam first

2. Get sponsorship from a FINRA member firm

3. Have your firm submit Form U4 through the Central Registration Depository

4. Schedule your exam within your 120-day enrollment window

5. Pay the $75 exam fee

The Series 63 process is a bit simpler:

1. Register through FINRA (no sponsorship technically required, though most people have one)

2. Schedule within your 120-day window

3. Pay the $147 exam fee

That 120-day window is no joke! If you miss it, your fee disappears and you’ll need to start over. Trust me, that’s not a mistake you want to make.

When exam day arrives, bring two forms of ID (one must be a government-issued photo ID) and show up at least 30 minutes early. You’ll need to stash all your personal belongings in the provided lockers – nothing goes into the testing room with you except your brain!

Need to reschedule? Do it at least 10 days before your appointment to avoid fees. Last-minute cancellations usually mean kissing your exam fee goodbye.

If at first you don’t succeed, you can try again after a 30-day waiting period. Same goes for a second failure. But if you don’t pass on your third attempt, you’ll be cooling your heels for a full 180 days before your next shot. And yes, you’ll pay the full fee each time – another good reason to pass on your first try!

Top Prep Resources & Study Hacks

The difference between passing and failing often comes down to how you prepare. Here are some resources that can make all the difference:

The official content outlines from FINRA and NASAA should be your starting point. They’re not exactly beach reading, but they tell you exactly what you need to know.

For practice questions, Kaplan’s SecuritiesPro™ QBank is worth every penny. Securities Training Corporation (STC) and ExamFX also offer excellent prep courses that many successful candidates swear by.

As for how to study, let me share some proven strategies:

Create flashcards for key terms – especially for the Series 63’s legal jargon. Your brain will thank you. Take timed practice exams to build your test-taking muscles and improve your pacing. Quiz yourself regularly instead of just re-reading material – this active recall is scientifically proven to strengthen your memory.

Space out your studying rather than cramming. Your brain forms stronger connections when you review material at increasing intervals. And don’t be shy about explaining concepts out loud – even if it’s just to your cat. Teaching something forces you to understand it more deeply.

Series 6 and Series 63: First-Try Pass Checklist

Want to nail both exams on your first attempt? Here’s your game plan:

Put in the hours – plan for 40-60 study hours for Series 6 and 30-50 hours for Series 63. This isn’t something you can cram for overnight.

Practice until you’re consistently scoring at least 80% on practice exams. When you can do this, you’re ready for the real thing.

Take the tutorial at the test center to get comfortable with the interface. Don’t worry – this 30-minute orientation doesn’t count against your exam time.

Get a good night’s sleep before the big day. Your brain works better with rest than with that extra hour of cramming.

Eat something substantial before heading to the test center. A grumbling stomach is a major distraction.

Arrive early, answer every question (there’s no penalty for wrong answers), and flag the tough ones to revisit if you have time at the end.

As one successful candidate told me, “Taking full practice tests under timed conditions was my secret weapon. By my third practice exam, I’d developed a rhythm that made the real test feel familiar. I passed both on my first try with confidence to spare.”

These exams are challenging but absolutely passable with the right preparation. Thousands of professionals successfully steer them every year – and you can too!

5. Keeping Your License Active

Once you’ve conquered the Series 6 and Series 63 exams, your journey is just beginning. Maintaining these valuable credentials requires ongoing attention and care – think of it like tending a garden rather than a one-and-done achievement.

Your hard-earned licenses have an expiration date of sorts. If you leave the industry and aren’t associated with a FINRA member firm for two years or more, your registrations become inactive. This “two-year rule” means the clock starts ticking the moment you step away from the industry.

“I’ve seen too many professionals have to retake exams because they didn’t realize how quickly that two-year window closes,” shares one compliance director. “It’s heartbreaking when they could have maintained their qualifications with minimal effort.”

Fortunately, regulators understand that life happens. The Series 63 offers flexibility through NASAA’s Exam Validity Extension Program (EVEP), which lets you maintain your Series 63 validity for up to five years even while not working at a financial firm. You’ll just need to complete annual continuing education requirements.

FINRA offers a similar lifeline with their Maintaining Qualifications Program (MQP) for the Series 6 and other FINRA exams. Both programs acknowledge that career pauses – whether for family care, health reasons, or other life circumstances – shouldn’t necessarily mean starting over from scratch.

Your ongoing education falls into two buckets:

-

Regulatory Element: This mandatory annual training covers regulatory updates, compliance standards, ethical practices, and sales guidelines. It’s non-negotiable and standardized across the industry.

-

Firm Element: This training is more personalized, focusing on the specific products and services you offer through your firm. The content and frequency vary depending on your employer and role.

“Continuing education isn’t just a box to check,” explains a veteran financial advisor. “It’s kept me ahead of regulatory changes that would have otherwise caught me off guard. I’ve even picked up sales strategies that have directly increased my client base.”

Renewal Costs & Deadlines

Keeping your Series 6 and Series 63 active involves a financial commitment and attention to important deadlines:

Your firm pays FINRA an annual assessment for each registered representative (that’s you!). While this happens behind the scenes, it’s good to be aware of it.

State registration fees vary widely, typically ranging from $50 to $200 per state annually. If you work with clients in multiple states, these fees can add up quickly, but they’re simply a cost of doing business.

Branch office registrations might trigger additional fees if you work in a registered branch location. Again, your firm usually handles these, but awareness is key.

Missing renewal deadlines can lead to painful late filing penalties and potential gaps in your registration status. Most renewals happen during FINRA’s annual renewal period in December.

While your firm’s compliance department typically manages these renewals, one compliance officer warned: “The most common mistake I see is representatives assuming their firm is handling everything. Always verify your registrations are current, especially if you’re registered in multiple states.”

Fingerprinting & Background Updates

Your initial registration required fingerprinting and a thorough background check, but your disclosure obligations continue throughout your career. You must update your Form U4 within 30 days of any material changes, including:

Personal matters like criminal charges or convictions, bankruptcy filings, judgments or liens, and even address changes need prompt reporting.

Professional issues such as customer complaints, arbitrations, and outside business activities must be disclosed quickly and completely.

These updates flow through FINRA’s Central Registration Depository (CRD) system and become publicly visible on FINRA’s BrokerCheck website. This transparency is non-negotiable in the financial industry.

The Financial Crimes Enforcement Network (FinCEN) rules may require updated fingerprints in certain situations, particularly when changing firms or returning after extended absences.

“Transparency isn’t just a regulatory requirement—it’s good business,” notes a securities attorney with 20 years of experience. “I’ve seen countless cases where disclosing issues proactively led to minor consequences, while hiding them resulted in career-ending penalties. The cover-up is almost always worse than the original issue.”

6. Career Paths After Passing

Congratulations! You’ve passed your Series 6 and Series 63 exams. Now what? These licenses aren’t just certificates to frame on your wall—they’re keys that open up a variety of exciting career doors in the financial services industry.

Many insurance professionals add these licenses to expand beyond traditional insurance products. With your Series 6 and Series 63, you can now offer clients variable annuities and variable life insurance—products with investment components that fixed insurance products simply don’t have.

“Adding my Series 6 transformed my practice,” shares Maria, an insurance agent from Denver. “Suddenly I could have deeper conversations about retirement planning and offer solutions that combined protection with growth potential.”

Banks love hiring professionals with these credentials too. As a bank investment representative, you’ll help customers move beyond savings accounts and CDs into mutual funds and annuities that might better serve their long-term goals. You’re essentially the bridge between traditional banking and wealth-building strategies.

Many mutual fund companies and financial institutions staff their call centers with Series 6 and Series 63 licensed professionals. While call center work might sound entry-level, it provides invaluable experience handling diverse client situations and questions. Plus, many senior advisors started their careers answering phones!

Financial planning firms often hire newly licensed individuals as paraplanners or junior advisors. In these roles, you’ll learn the business from experienced planners while handling client service tasks and building your knowledge base. It’s a perfect training ground for eventually managing your own client relationships.

If you enjoy teaching others about investments, consider becoming a mutual fund wholesaler. Rather than working with retail clients, you’ll educate financial advisors about your company’s fund offerings. It’s a great role for those who love the technical aspects of investments and have strong presentation skills.

With experience and additional licensing (particularly the Series 26 Principal Exam), supervisory roles become possible. Managing a team of representatives can be both challenging and rewarding, with compensation that reflects your increased responsibilities.

The financial outlook is promising too. According to the Bureau of Labor Statistics, securities sales agents earned a median annual wage of $62,910 in 2021, with projected job growth of 10% through 2031. Personal financial advisors did even better, with a median salary of $94,170 and projected growth of 15%.

“The Series 6 and Series 63 are often stepping stones,” explains Tom, a career counselor in financial services. “I’ve seen people start in call centers with just these two licenses and eventually become successful financial planners with six-figure incomes. Your career path is really what you make of it.”

Comparing to Other Licenses

While your Series 6 and Series 63 provide a solid foundation, you might eventually want to add other licenses to expand your capabilities.

The Series 7 (General Securities Representative) license is broader than the Series 6, allowing you to sell individual stocks, bonds, options, and other securities beyond packaged products. Many professionals view it as a natural upgrade from the Series 6. It requires passing the SIE first, consists of 125 questions over 3 hours 45 minutes, and costs $300.

If you’re interested in providing fee-based investment advice rather than just selling products, the Series 65 (Uniform Investment Adviser Law Examination) is your ticket. It requires no prerequisites or sponsorship, has 130 questions over 3 hours, and costs $187. This license lets you charge clients directly for your advice instead of relying solely on commissions.

The Series 66 (Uniform Combined State Law Examination) efficiently combines Series 63 and Series 65 content for those who already hold the Series 7. With 100 questions over 2 hours 30 minutes and a $177 fee, it’s a streamlined option that saves time for Series 7 holders.

Many financial professionals follow a natural progression: starting with Series 6 and Series 63 (for mutual funds and variable products), adding Series 7 (for all securities products), then Series 65 or 66 (for fee-based advisory services), and potentially supervisory licenses like the Series 24 or 26.

“I started with just the 6 and 63 twenty years ago,” shares Robert, a veteran financial advisor. “As my practice evolved, I added the 7, then the 65, and eventually the 24 to supervise others. Each license expanded what I could offer clients and increased my earning potential.”

Your new licenses aren’t the destination—they’re the beginning of what could be a rewarding, dynamic career helping people achieve their financial goals. The path you take from here depends on your interests, strengths, and the specific client needs you most enjoy addressing.

Frequently Asked Questions about Series 6 and Series 63

Do I need to pass the SIE before both exams?

The pathway to getting licensed can sometimes feel like navigating a maze, especially when it comes to prerequisites. Here’s the straightforward answer: You only need to pass the Securities Industry Essentials (SIE) exam before taking the Series 6 exam—not the Series 63.

This requirement kicked in back in October 2018 when FINRA restructured their examination program. The SIE covers those fundamental securities concepts that every professional should know, regardless of their specific role in the industry.

The Series 63, on the other hand, stands on its own with no prerequisites. You could technically take it first if you wanted to. But here’s the catch—the Series 63 by itself won’t let you sell securities. You’ll still need a FINRA qualification exam like the Series 6 or Series 7 to actually conduct business.

Most people follow a logical sequence: SIE first, then Series 6, and finally Series 63. But if you’re eager to knock out the state law requirements, you could absolutely take the Series 63 earlier in your journey.

How much do the exams cost and who pays?

Let’s talk dollars and cents. Here’s what you’re looking at for exam fees:

– SIE: $80

– Series 6: $75

– Series 63: $147

As for who covers these costs—it varies widely across the industry. Many larger broker-dealers view these fees as an investment in their team and will cover them entirely for new hires. As one hiring manager told me, “We pay for all licensing costs, but we do ask our new advisors to commit to at least a year with us in return.”

Smaller or independent firms might take a different approach. Some will reimburse you after you pass (extra motivation!), while others might wait until you’ve been with them for a certain period.

If you’re one of the rare self-sponsored candidates for the Series 6 or the more commonly self-sponsored Series 63 takers, you’ll be covering these costs yourself.

Don’t forget about study materials too. These can range from about $100 for basic self-study guides to $500+ for comprehensive packages that include instructor support and interactive practice exams. While not required, good study materials are often the difference between passing on your first try or paying for a retake.

Are remote (online) testing options available?

The testing landscape has evolved significantly in recent years. Traditionally, you’d need to physically go to a Prometric testing center to take both the Series 6 and Series 63 exams. The testing room, the check-in process, the lockers for your belongings—it was all part of the experience.

Then the pandemic changed everything. FINRA introduced online testing options for certain exams through Prometric’s ProProctor platform, allowing candidates to take tests from home. However, the availability of remote testing continues to evolve based on regulatory decisions.

If you’re hoping to test remotely, you’ll need:

– A private, quiet room where you won’t be disturbed

– A computer with a functioning webcam and microphone

– A reliable internet connection

– Your government-issued photo ID

– Patience for the virtual check-in process, which includes a thorough scan of your testing environment

“I took my Series 63 remotely during the height of the pandemic,” one test-taker shared with me. “Don’t be fooled into thinking it’s more relaxed than a testing center. The online proctors are watching your every move through the webcam, and they’re just as strict about the rules. They even made me show them under my desk and do a complete room scan before starting.”

For the most current information about remote testing availability, I’d recommend checking the official FINRA and NASAA websites, as these options can change quickly as regulations evolve.

Conclusion

Navigating Series 6 and Series 63 licensing might seem daunting at first, but with the right preparation and mindset, these credentials can become powerful tools in your financial services career. These licenses aren’t just regulatory requirements—they’re your ticket to helping clients achieve their financial goals through mutual funds, variable annuities, and other investment products.

Looking back at what we’ve covered, a few key points stand out:

The Series 6 equips you to sell packaged investment products like mutual funds and variable annuities, opening doors to roles in banks, insurance companies, and financial planning firms. You’ll need to pass the SIE exam first before tackling this one.

The Series 63 focuses on state securities laws (those famous “Blue Sky” regulations) and gives you the freedom to conduct business across state lines. While eight states don’t require it, having this license in your back pocket provides valuable flexibility as your career grows.

Most professionals in our industry need both licenses to effectively serve clients and build a sustainable practice. They complement each other beautifully—one focuses on products, the other on where you can sell them.

I’ve seen countless professionals transform their careers with these credentials. One advisor told me, “Getting my Series 6 and 63 was like being handed the keys to a new car—suddenly I could take clients places they needed to go for their financial futures.”

Maintaining your licenses requires ongoing attention to continuing education requirements and registration renewals. Think of it as regular maintenance on that car—neglect it, and you might find yourself stranded!

At Ironclad Law, we understand that securities licensing is just one piece of your compliance puzzle. Our team takes an aggressive approach to protecting your professional interests, whether you’re just starting your journey or looking to expand your credentials further.

We’ve guided countless financial professionals through the complexities of FINRA regulations and state securities laws. Our hands-on approach means you’ll never face regulatory challenges alone. We’re with you from exam preparation through ongoing compliance support, helping you steer the ever-changing regulatory landscape with confidence.

Proper licensing isn’t just about checking regulatory boxes—it’s about building trust with clients and creating a foundation for a successful, sustainable career in financial services. When clients know you’ve invested in yourself through proper licensing, they’re more likely to trust you with their financial futures.

Ready to take the next step in your securities licensing journey? We’re here to help.